The US Dollar Currency Index (DXY) measures the relative value of the US dollar against a basket of other foreign currencies.

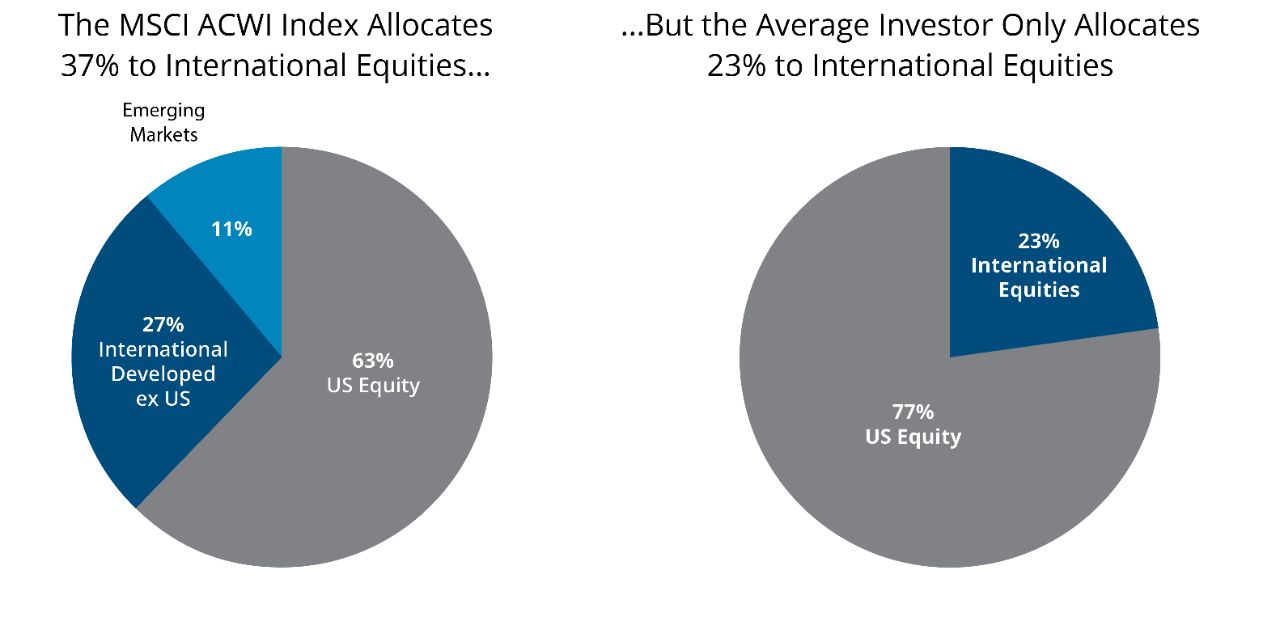

MSCI ACWI Index is a free float-adjusted market capitalization index that measures equity market performance in the global developed and emerging markets.

MSCI ACWI ex USA Index is a free float-adjusted market-capitalization index thatthat measures the performance of both developed and emerging stock markets, excluding the United States.

MSCI World ex USA Index is a free float-adjusted market capitalization index that captures large- and mid-cap representation across developed markets countries excluding the United States.

S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks.

Important Risks: Investing involves risk, including the possible loss of principal. • Foreign investments may be more volatile and less liquid than US investments and are subject to the risk of currency fluctuations and adverse political, economic, and regulatory developments. These risks may be greater, and include additional risks, for investments in emerging markets or if a fund focuses in a particular geographic region or country. • Different investment styles may go in and out of favor, which may cause a Fund to underperform the broader stock market. • To the extent a Fund focuses on one or more sectors, the Fund may be subject to increased volatility and risk of loss if adverse developments occur. • Diversification and asset allocation do not ensure a profit or guarantee against loss.

The views expressed here are those of the author. They should not be construed as investment advice. They are based on available information and are subject to change without notice. This material and/or its contents are current as of the time of writing and may not be reproduced or distributed in whole or in part, for any purpose, without the express written consent of Hartford Funds.