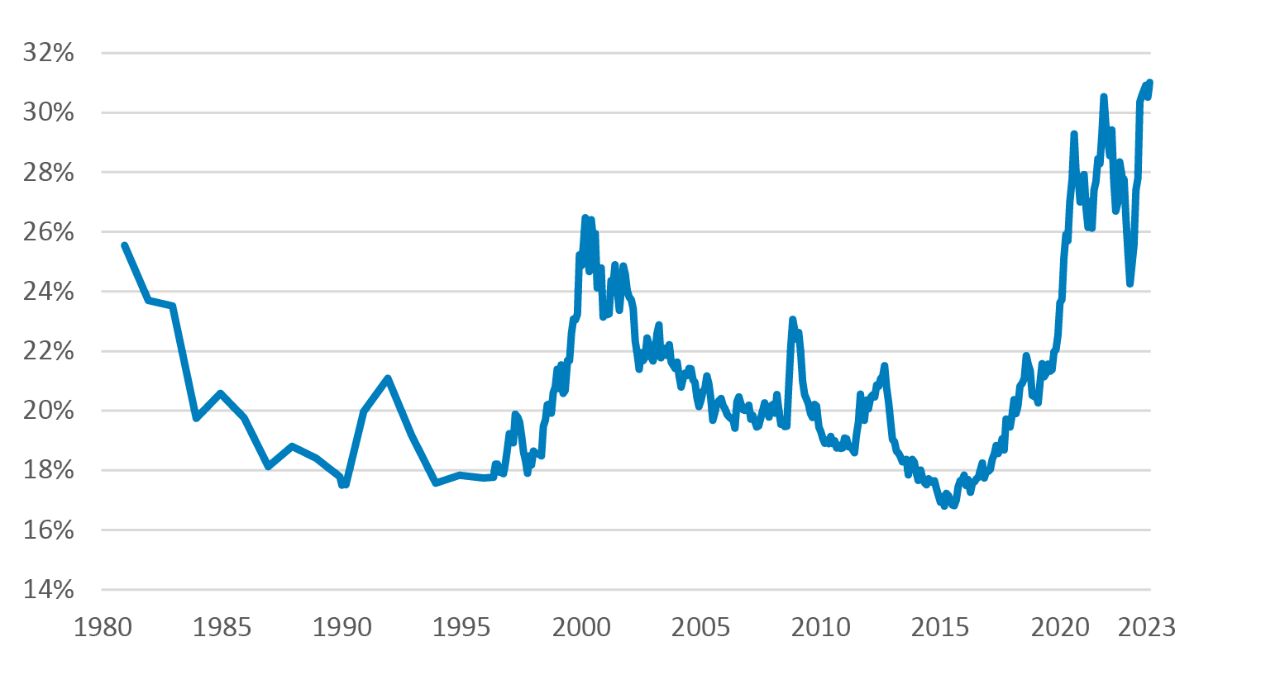

Global stock markets have become increasingly top-heavy. At the end of October, the 10 biggest stocks in the S&P 500 Index1 made up a record 31% of the market (FIGURE 1). For investors trying to build diversified portfolios, this presents an issue, as a significant proportion of their risk is being driven by a relatively small number of companies.

Our research shows that, historically, investors passively tracking the US stock market would have lost out on returns in the years following high levels of index concentration. At a time when investors are increasingly allocating to passively managed strategies at the expense of active, the tables could be set to turn.

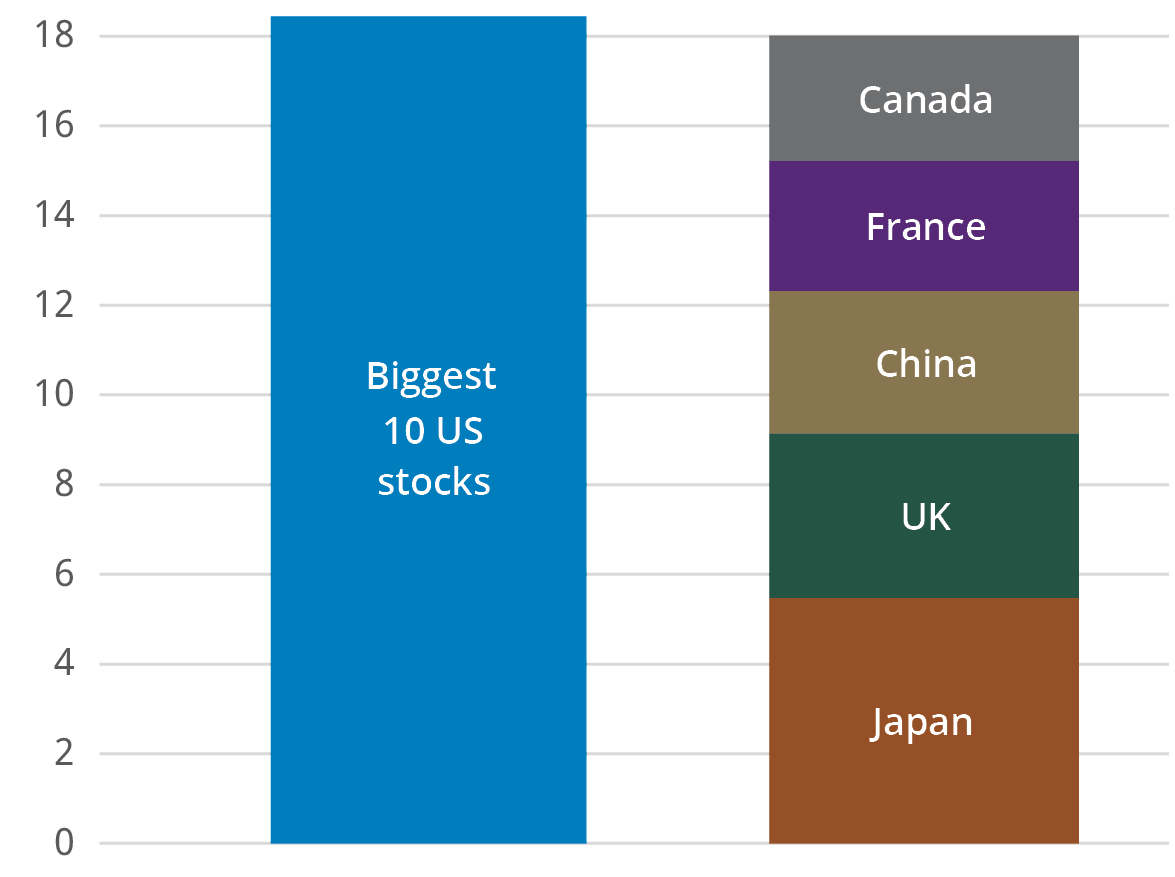

This isn’t just an issue for the US stock market: The US has grown to be 63% of the global market at the end of October (MSCI ACWI Index)2—so international investors have ended up with a lot of exposure to US stocks and, more so, a lot of exposure to just 10 stocks. Those 10 stocks make up nearly 18% of the global market—the same as Japan, the UK, China, France, and Canada combined (FIGURE 2).