Pre-Sales Support

Mutual Funds and ETFs - 800-456-7526

Monday-Thursday: 8:00 a.m. – 6:00 p.m. ET

Friday: 8:00 a.m. – 5:00 p.m. ET

Post-Sales and Website Support

888-843-7824

Monday-Friday: 9:00 a.m. - 6:00 p.m. ET

If you’re worried about the future of your Social Security benefits, you’re not alone. Seventy-two percent of adults worry that Social Security will run out of funding in their lifetime.1 This concern is shared by both workers expecting to rely on these benefits someday and retirees currently receiving payments.

It’s no wonder they’re concerned. Social Security’s financing issues and a steady stream of headlines such as “Social Security Trust Funds Projected to Be Depleted in 2032”2 can put us on edge. Unfortunately, they can also lead people to claim their benefits early—which could have significant long-term effects on their financial well-being.

While Social Security is unlikely to disappear, it may undergo changes. Nevertheless, you can take proactive steps now to prepare for potential changes and protect your future retirement income.

First, Is Social Security Really Going Away?

Social Security is one of the most popular and successful federal programs in US history and offers retirees a reliable income stream to help sustain their standard of living.

Therefore, neglecting the program, or allowing it to deteriorate, could provoke voter backlash, which politicians are keen to avoid. Rather than large, sweeping reforms, politicians are more inclined to address it with small, incremental changes necessary to shore up the program. Several proposed changes, if enacted, could bolster Social Security in the long run. But any changes would take time to become apparent and likely wouldn’t be felt for at least a decade.3

Even in the unlikely event that Congress doesn’t act before funds are depleted, Social Security wouldn’t go bankrupt. Ongoing Federal Insurance Contributions Act (FICA) payroll tax revenue would still fund about 80% of promised benefits indefinitely.3

Second, The Pitfalls of Panic

Despite this, many individuals file for benefits before full retirement age, resulting in lower payments. A common misconception is that these payments will automatically increase to 100% of the full retirement benefit amount when full retirement is reached.

This is not the case.

Filing early locks in reduced benefits for life. Not only are individual benefits reduced, but spousal benefits are, too. Delaying benefits may result in a higher monthly payout for both individuals and spouses.

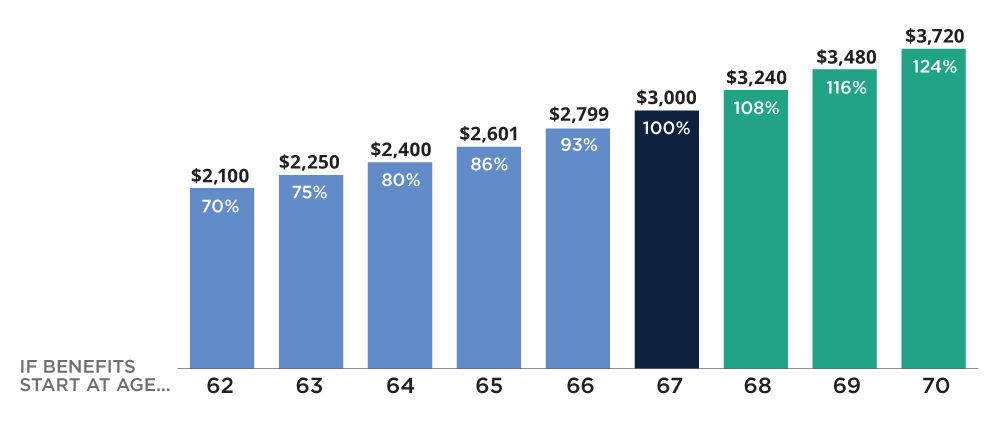

Early vs. Delayed Filing: How it Affects Your Social Security Benefit4

The chart above assumes a full retirement age of 67, when an individual would receive 100% of their benefit. Filing early results in a reduced benefit, but the longer it’sdeferred, the greater the benefit. You can defer your benefit until age 70. For illustrative purposes only. Actual benefits will vary. Source: SSA.gov

How Filing Early Could Affect Your Benefits

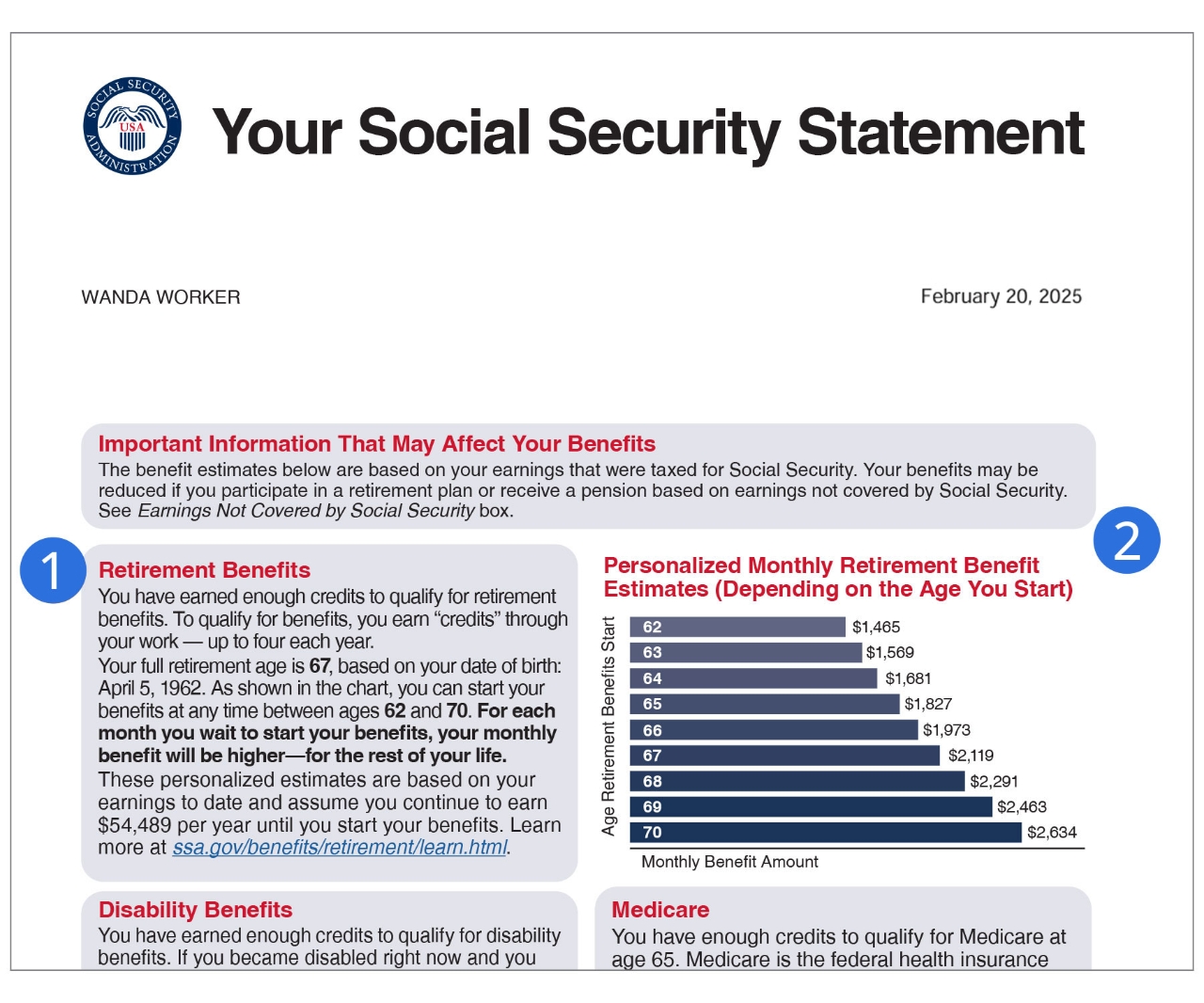

To understand how filing early or delaying might affect your benefits, check your Social Security Statement online at www.ssa.gov/myaccount. If you don’t have an account yet, you can easily create one.

Review your statement for two key pieces of information:

Source: Your Social Security Statement, ssa.gov, 2025

Even if you receive your maximum Social Security benefit it likely won’t be enough to cover all of your retirement expenses. That’s why personal retirement planning remains important.

Third, Identifying Other Retirement Income Sources

Your financial professional can help you identify your retirement-income sources in addition to your Social Security. This will help you determine how each one fits into your overall retirement income plan. These sources may include:

To provide comprehensive planning and help optimize your investments, your financial professional needs to be aware of all your accounts. For instance, if you have multiple IRAs in different places, it might be wise to consult your financial professional and a tax professional about consolidating these and other accounts if appropriate. Your financial professional can estimate potential retirement income from these and other sources, giving you a clearer financial picture.

To Summarize

While Social Security funding may be strained, the program isn’t going away, and filing early out of fear can significantly reduce both individual and spousal benefits. Taking an inventory of your retirement-income sources can help provide valuable perspective.

Social Security FOMO May Scare People Into Filing Early, Which Can Backfire

When making Social Security decisions, it’s crucial to stay calm and informed, rather than letting fear dictate your choices. Acting out of fear can lead to decisions that may do more harm than good. You’ll need to weigh the pros and cons of filing early vs. waiting, considering factors such as your life expectancy, other income sources, and tax implications. While this may seem overwhelming, your financial professional can help you navigate these decisions.

Next Step

Talk to your financial professional about how Social Security income fits into your overall financial plan.

Mike is a managing director of the Hartford Funds Applied Insights Team. The team translates the expertise of the psychologists, physiologists, professors, and practice-management experts we partner with into practical, actionable ideas and tools to make sense of a rapidly evolving market and demographic landscape.

1 More than three in four US adults believe the Social Security system needs to change.Nationwide, 7/24.

2 2026 OASDI Trustee Report

3 Social Security in 2024 and Beyond, marybethfranklin.com, 12/23.

4 When to Start Receiving Retirement Benefits, Publicatio No. 05-10147, ssa.gov, 5/24

All information provided is for informational and educational purposes only and is not intended to provide investment, tax, accounting, or legal advice. As with all matters of an investment, tax, or legal nature, you should consult with a qualified tax or legal professional regarding your specific legal or tax situation, as applicable.