HALF

of parents

|

|

Mark is 64 and starting to think seriously about retirement. His daughter, Kayla, is 29.

A couple of years ago, when Kayla lost her job, Mark stepped in to help with rent. It was meant to be temporary.

But even after she found work, the support didn’t stop. First rent, then her cell phone, then car insurance. Each time something came up, Mark filled the gap.

Now, it’s simply what he does. They’ve never talked about when—or if—it ends.

Lately, Mark has been thinking about pulling back. But every time he does, the same worries start to creep in:

What if she can’t make it on her own?

What if she falls behind or goes into debt?

What if she loses her apartment?

What if this damages our relationship?

So, he keeps helping. And tells himself he’ll deal with it later.

At the same time, he’s beginning to notice something else: the continued support is taking a toll on his retirement savings—and it’s getting harder to ignore.

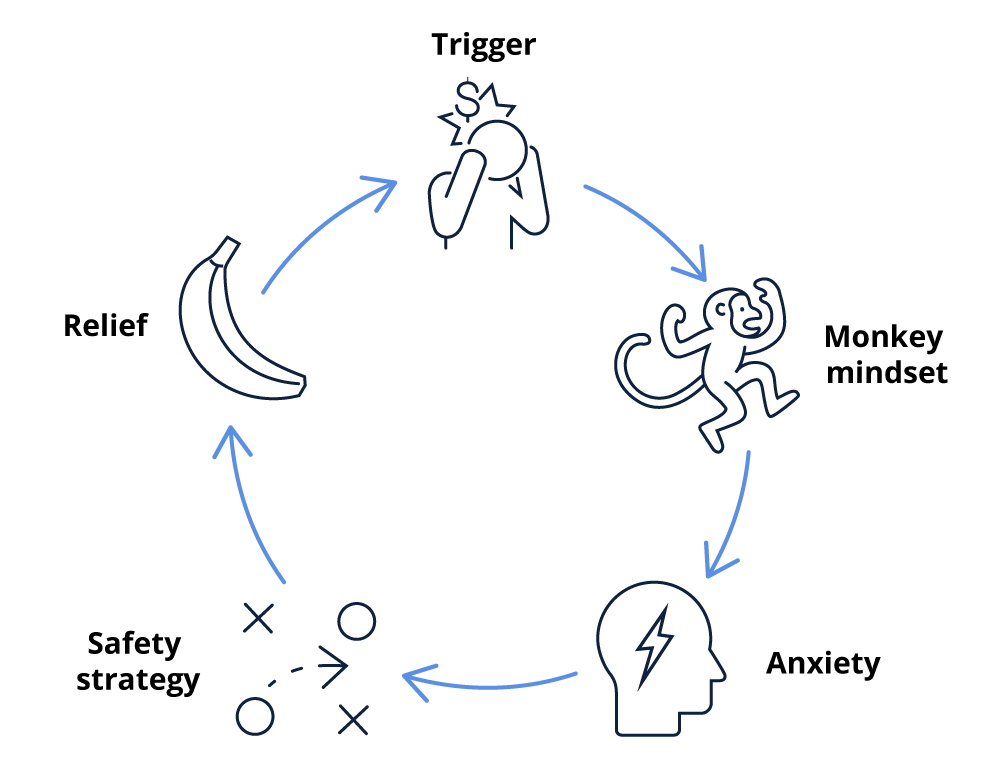

In my practice, I see this pattern often. Temporary support can quietly become an open-ended commitment—one that may be emotionally difficult to unwind.

Fortunately, there’s a way to better understand what’s driving this dynamic—and how to begin shifting it.

First, How Good Intentions Can Put Your Retirement at Risk

Let’s start with an important distinction: not all financial support is harmful.

Many parents provide thoughtful, intentional help—and it can be part of a healthy financial plan.

For example:

- Helping fund a degree or vocational training with a clear endpoint

- Providing support during a job loss or life transition, with a plan to phase it out

- Contributing in a way that’s mutually understood and doesn’t disrupt long-term goals

This kind of support is purposeful, time-bound, and aligned with a broader plan.

But there’s another pattern I see more often.

It starts in a similar place—but gradually becomes ongoing, open-ended, and harder to step back from.

I call this over-responsibility—the belief that you are responsible for everyone’s happiness and safety.

When that belief is in play, financial decisions can shift. What looks like generosity on the surface is often driven by a deeper sense that you have to help.

This can show up as:

- Covering ongoing living expenses without revisiting the plan

- Stepping in quickly at the first sign of struggle

- Continuing support even as it begins to affect your own financial future

The question isn’t whether helping is right or wrong.

It’s this:

- Is this support part of a plan?

- Or has it become something you feel responsible for maintaining—no matter the cost?