Pre-Sales Support

Mutual Funds and ETFs - 800-456-7526

Monday-Thursday: 8:00 a.m. – 6:00 p.m. ET

Friday: 8:00 a.m. – 5:00 p.m. ET

Post-Sales and Website Support

888-843-7824

Monday-Friday: 9:00 a.m. - 6:00 p.m. ET

John Hennigan, a professional poker player in Vegas, wondered what it would be like to live in Des Moines, Iowa. He bet some fellow poker players $30,000 that he could leave the poker table, jet to Des Moines, and live there for a month. His poker buddies knew that Hennigan enjoyed the high-stakes poker lifestyle, and doubted he could handle the quieter pace of Des Moines. His friends were right. After two days, Hennigan agreed to pay $15,000 to get out of the bet.

Des Moines wasn’t a good fit for him.

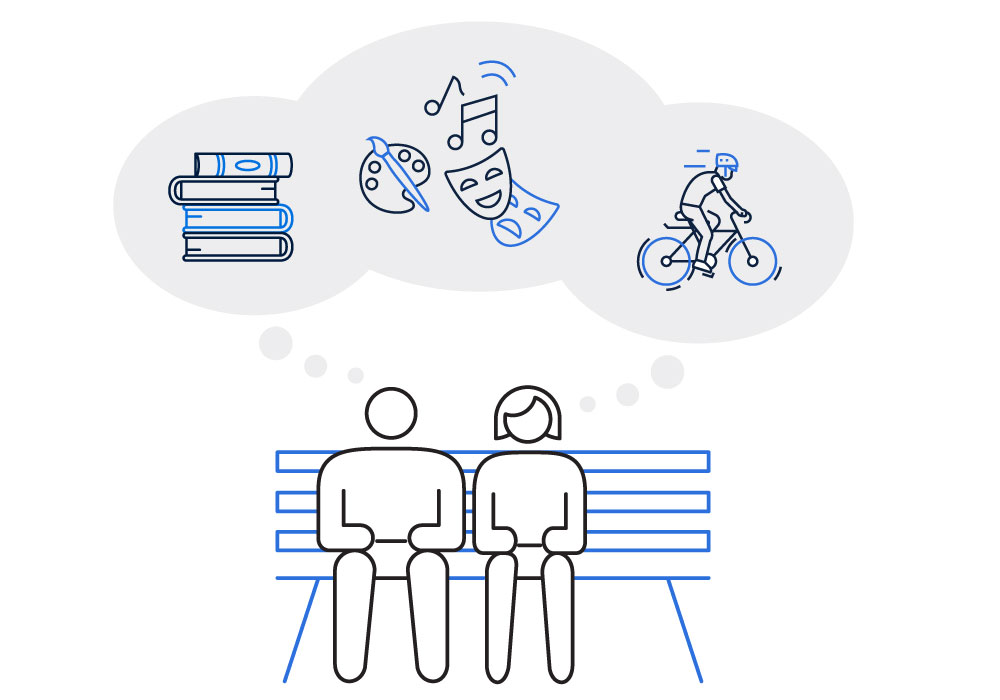

Unlike Hennigan’s experience, the location you choose for retirement needs to be a good fit. Many retirees are finding some unexpected advantages in college towns. You might not think that a town full of 18-22 year olds would be an ideal retirement location, but college towns can be a great place for retirement. What makes them a good fit for retirees? It’s the advantages of accessibility, great healthcare, and an array of activities to meet a variety of interests.

Why College Towns Can Be Great Places for Retirement

Access to Learning

Cultural Events

Easy to Get Around

First, Some College Towns Are Prepped for Retirees

If learning during retirement is a priority for you, then you might consider retiring near a college. But with more than 5,700 colleges in the US,1 how would you decide? You could check out University Based Retirement Communities (UBRCs)—privately-owned retirement communities in college towns. They typically have an affiliation with a nearby college and are designed to benefit retirees. These communities offer retirees the opportunity to attend classes and university activities, such as guest lectures, concerts, and cultural or sporting events.

There Are Over 100 University-Based-Retirement Communities in the US Today

There isn’t a set standard of criteria that all these communities follow. The list below was developed by Andrew Carle, assistant professor at George Mason University and an expert in these communities. You could use these general guidelines to evaluate UBRC choices:

Not all UBRCs meet all the criteria, so you’ll need to do your homework to understand what programs and services each one provides. You can also consider retirement communities that are located near a college but not affiliated with it—or simply living in a private residence near a college town. Either way, the concept is based on the notion that even people of retirement age are interested in what colleges and college towns provide.

Second, Organizations That Make Access to Learning Easy

Many popular retirement communities are in scenic locations with golf courses nearby. Think about what people do for recreation there. What comes to mind? Were you thinking bingo, movie night, or card games?

College towns can offer some or all of those same activities, as well as quality, diverse intellectual opportunities. And some organizations make learning available without the typically high cost of college courses. Lifelong Learning Institutes are affiliated with colleges and offer non-credit, college-level educational experiences for older adults, but with little or no homework and at a fraction of the cost. The institute’s classes are taught by members, retired and active faculty, and outside experts.

Osher Lifelong Learning Institutes also offer a distinctive array of non-credit courses and activities specifically developed for adults age 50 or older who are seeking intellectual enrichment. These institutes can be found on campuses of 123 colleges and universities. UBRCs typically allow retirees to audit classes at nearby colleges, which means that retirees can attend classes for free without receiving credits. If you’re considering one of these communities, ask about the availability of courses. Some communities don’t provide access to all courses, or they may offer them on a space-available basis. Lasell Village, a UBRC in Newton, Massachusetts, takes lifelong learning to a whole new level: they require it. Residents are required to complete 450 hours of learning and fitness activities every year.

On Campuses, You’ll Find Plenty of Cultural Events

If you live in proximity to a college campus, you have access to plays, recitals, concerts, lectures, and art galleries. For example, the UBRC Kendal at Hanover in New Hampshire offers retirees access to over 500 events in film, dance, music, and theater each year on the Dartmouth University campus. There are also major sporting events including basketball, football, and lacrosse, among others. College sporting and cultural events are relatively inexpensive and some may even be free.

Another benefit of retiring to a college town versus a traditional retirement community is the opportunity to mingle and socialize with younger people. In addition to interacting with younger students in classes, you can find volunteer opportunities on campus, such as mentoring other students. Conversely, college students often volunteer at the UBRCs. For example, computer science majors may do one-on-one computer training with retirees, or students in the art department may lead ceramics or painting workshops.

Third, It’s Easy to Get Around

Early in retirement, driving is usually feasible for retirees. But as the years roll by, driving can become a challenge. When this happens, retirees often rely on family to shuttle them around. Depending on where retirees live, options such as public transportation, taxis, or Uber and Lyft may or may not be available.

Because lots of students don’t have cars on campus, most things students need are within walking distance. That’s good news for retirees who have driving limitations. They can usually walk to the campus, restaurants, and stores. And if you like to walk for exercise, there are lots of walking and biking trails in college towns.

College towns also offer reliable public and private transportation options. If you live in a retirement community in a college town, transportation to the campus and other popular locations are typically available. And pay-for-ride options, like Uber or Lyft, are usually available in minutes. Plus you can get food from local restaurants delivered to you using services like Grubhub. College towns give you easy access to the things you want and need.

Would You Feel Out of Place on Campus?

College towns aren’t always a good fit for retirees. It’s natural to feel awkward entering a classroom filled with a bunch of younger students. But most residents in UBRCs want to keep learning, so you’d likely be attending classes with fellow retirees. This can alleviate those awkward feelings. If you’re still not sure you’d fit in, you might be able to find a place to rent at SabbaticalHomes.com to get a feel for the lifestyle.

This option, which isn’t limited to professors and academics, gives you the chance to live in a college town for a year or so before deciding to make a long-term commitment. Remember These Things if You’re Considering a College Town for Retirement First, remember that some college-town communities are better suited for retirees than others. UBRCs typically have affiliations with colleges and are specifically designed to benefit retirees. Second, find out what educational and cultural opportunities are available in the communities you’re considering. Third, do a bit of time traveling. Imagine a time in your future when you couldn’t drive. How would that impact your life? Realize that communities in college towns tend to offer lots of transportation alternatives.

Some Retirees Want More Than a Leisure-Filled Retirement

When we think of the typical retirement community, we often envision aging adults engaging in leisure-focused activities. But some retirees envision something else. Retirees are finding that college towns offer unexpected advantages, such as lifelong learning, cultural experiences and interaction with younger generations. If college towns sound enticing, do your homework. You don’t want to regret the move like John Hennigan did.

Next Steps

| 1 | Consider how important life-long learning is to your retirement |

| 2 | Find a list of top-rated UBRCs at A Place for Mom |

| 3 | If you’re not ready to move to a college town, find free or low-cost college classes for aging adults in your state by googling Free & Cheap College Classes for Senior Citizens at Money Crashers |

Financial Professionals |

This article is based off of our popular 8,000 Days module. Click here to access additional content to share.

Source:

1 College Statistics By States, UNIVSTATS, 2025

2 Pricey but Good for the Brain: University Retirement Communities, Rate.com, 8/31/20

Hartford Funds may or may not be invested in the companies referenced herein; however, no particular endorsement of any product or service is being made.