Pre-Sales Support

Mutual Funds and ETFs - 800-456-7526

Monday-Thursday: 8:00 a.m. – 6:00 p.m. ET

Friday: 8:00 a.m. – 5:00 p.m. ET

Post-Sales and Website Support

888-843-7824

Monday-Friday: 9:00 a.m. - 6:00 p.m. ET

So far in 2023, S&P 500 Index1 returns exhibit a healthy and robust stock market, with a 16.89% return through the end of June.2 Looking under the hood, though, the story shifts to a very narrow, concentrated market that lacks breadth.

Just seven mega-cap companies have accounted for about 75% of the Index’s returns year-to-date (YTD) (FIGURE 1). At the close of the second quarter, these seven stocks—also known as the Magnificent Seven—accounted for nearly one-third of the Index by weight and are the top-seven stocks by market cap.

FIGURE 1

Just Seven Companies Are Driving S&P 500 Index Returns

S&P 500 Index Mega-Cap Company Returns YTD

| Returns YTD (%) | |

| Apple | 49.65 |

| Microsoft | 42.57 |

| Nvidia | 189.52 |

| Amazon | 55.19 |

| Meta | 138.47 |

| Tesla | 112.51 |

| Alphabet | 35.67 |

As of 6/30/23. Source: Morningstar Direct.

Not all these stocks fall within the information-technology sector, but they’re almost always collectively referred to as “big tech” due to their sheer size and innovation impact. While these businesses are quite different, they tend to move up and down in sync, which can have a sizable impact on the direction of market-cap weighted indices and products.

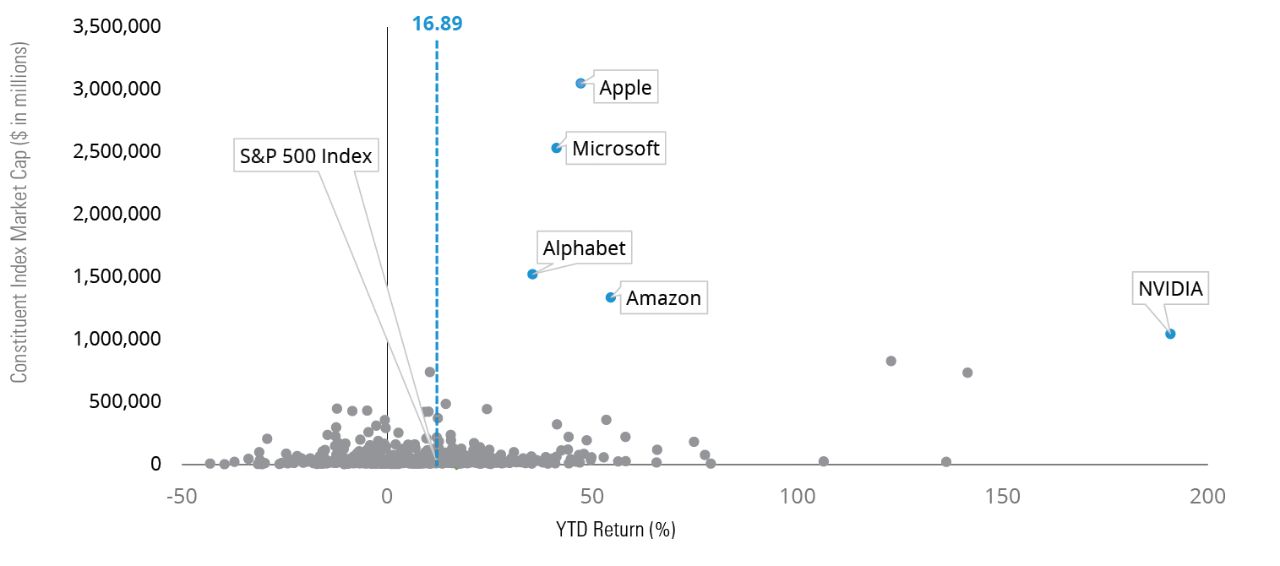

To illustrate how narrow performance has been in the S&P 500 Index YTD, FIGURE 2 plots constituents by market cap and YTD returns. Of the 503 companies in the Index, 74% are underperforming the Index’s total return, and 40% have experienced flat-to-negative performance YTD.

FIGURE 2

Market Performance Is Being Driven by a Handful of Companies

YTD Market-Cap Exposure and Return (%) for S&P 500 Index Companies

As of 6/30/23. Past performance does not guarantee future results. Investors cannot directly invest in indices. The S&P 500 Index’s seven largest companies as measured by free-float market capitalization. Data sources: FactSet and Hartford Funds, 7/23.

Nasdaq is also facing this top-heavy concentration. In July, the Nasdaq 100 Index3 underwent a “special rebalancing” after the Magnificent Seven exceeded a stipulated threshold, triggering the process. The rebalancing is meant to reduce the degree to which Index performance is determined by a small number of stocks—taking some of the portfolio weight from the largest stocks and redistributing it among the other Index constituents. On July 3, the top-seven stocks made up 55% of the Index’s weighting. Following the rebalance, it dropped to about 43%.4

Big tech has benefited from the recent boom in artificial intelligence, declining inflation, and optimism that the Federal Reserve is nearing the end of its rate-hiking campaign. But is the exceptional performance from tech-heavy hitters sustainable?

Takeaways

To learn more about the role of diversification in your portfolio, talk to your financial professional.

1 S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks.

2 As of 6/30/23. Source: Morningstar Direct.

3 The Nasdaq 100 Index is a stock index of the 100 largest companies by modified market capitalization trading on Nasdaq exchanges.

4 Nasdaq, “Nasdaq-100 Rebalance: What ETF Investors Should Know,” 7/24/23.

Important Risks: Investing involves risk, including the possible loss of principal. • Diversification does not ensure a profit or protect against a loss in a declining market. • Small- and mid-cap securities can have greater risks and volatility than large-cap securities. • Foreign investments, including foreign government debt, may be more volatile and less liquid than US investments and are subject to the risk of currency fluctuations and adverse political, economic and regulatory developments.

The views expressed here are those of the author and should not be construed as investment advice. They are based on available information and are subject to change without notice. Portfolio positioning is at the discretion of the individual portfolio management teams; individual portfolio management teams, and different fund sub-advisers, may hold different views and may make different investment decisions for different clients or portfolios. This material and/or its contents are current as of the time of writing and may not be reproduced or distributed in whole or in part, for any purpose, without the express written consent of Hartford Funds.