Pre-Sales Support

Mutual Funds and ETFs - 800-456-7526

Monday-Thursday: 8:00 a.m. – 6:00 p.m. ET

Friday: 8:00 a.m. – 5:00 p.m. ET

Post-Sales and Website Support

888-843-7824

Monday-Friday: 9:00 a.m. - 6:00 p.m. ET

Remember how you rode your bike as a kid? You aimed for every pothole, launched off every ramp, and never wore a helmet. Now you avoid the bumps and look for a smooth ride. Investing follows the same arc: Younger clients can absorb more risk, but as they age, reducing risk becomes the priority.

That’s where we’re headed as a country. The aging of the US population is reshaping asset allocation and portfolio construction as investors seek to reduce risk.

Four structural tailwinds suggest fixed-income demand has room to grow regardless of where financial markets or interest rates are headed.

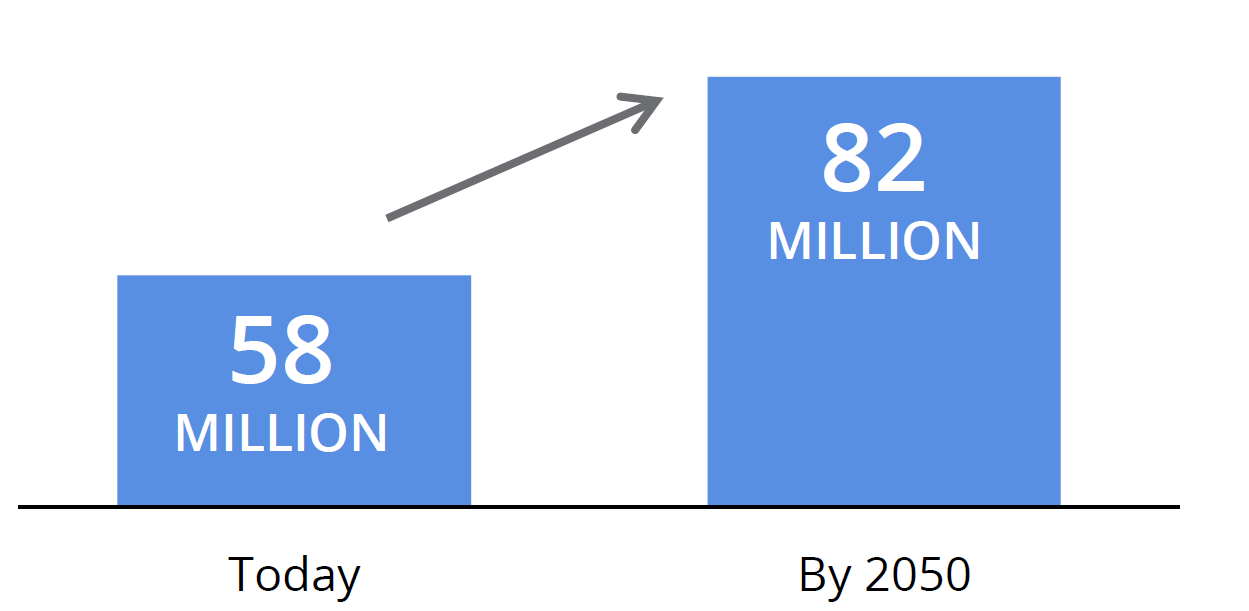

1. The Retirement Age Wave Is Here

The number of Americans age 65+ is projected to rise by 42% from 58 million to 82 million by 2050.

Current vs. Projected Number of Americans Age 65+

Projections are from 2022 (most recent data available). Data Source: Population Reference Bureau, Fact Sheet: Aging in the United States.

As investors age, bonds tend to play a larger role in portfolios—supporting income, helping preserve capital, and smoothing out volatility. That shift becomes even more important after age 65, when recovering from large drawdowns becomes more challenging.

Recovering from large drawdowns becomes more challenging after age 65.

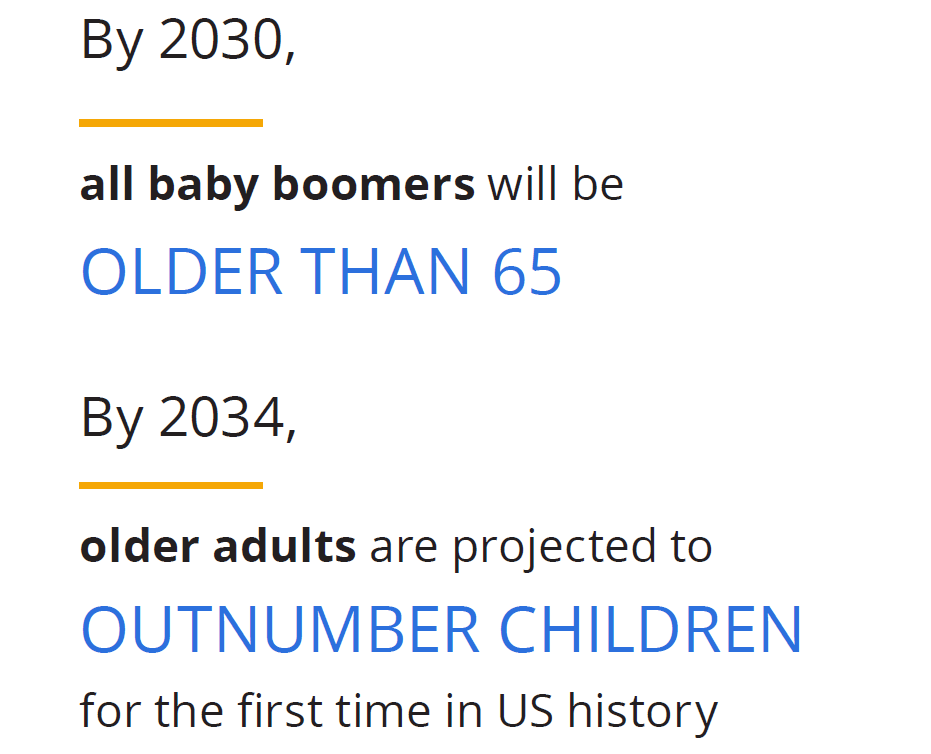

2. The 2030s Will Bring Two Significant Demographic Milestones

Some demographic trends move so slowly that they don’t have a meaningful impact on markets. That’s not the case for the two trends we’ll experience in the 2030s.

Data Sources: US Census Bureau, Demographic Turning Points for the United States: Population Projections for 2020 to 2060.

These milestones don’t call for immediate action for every investor, but they do make the shift harder to ignore as it begins to show up more clearly across the economy.

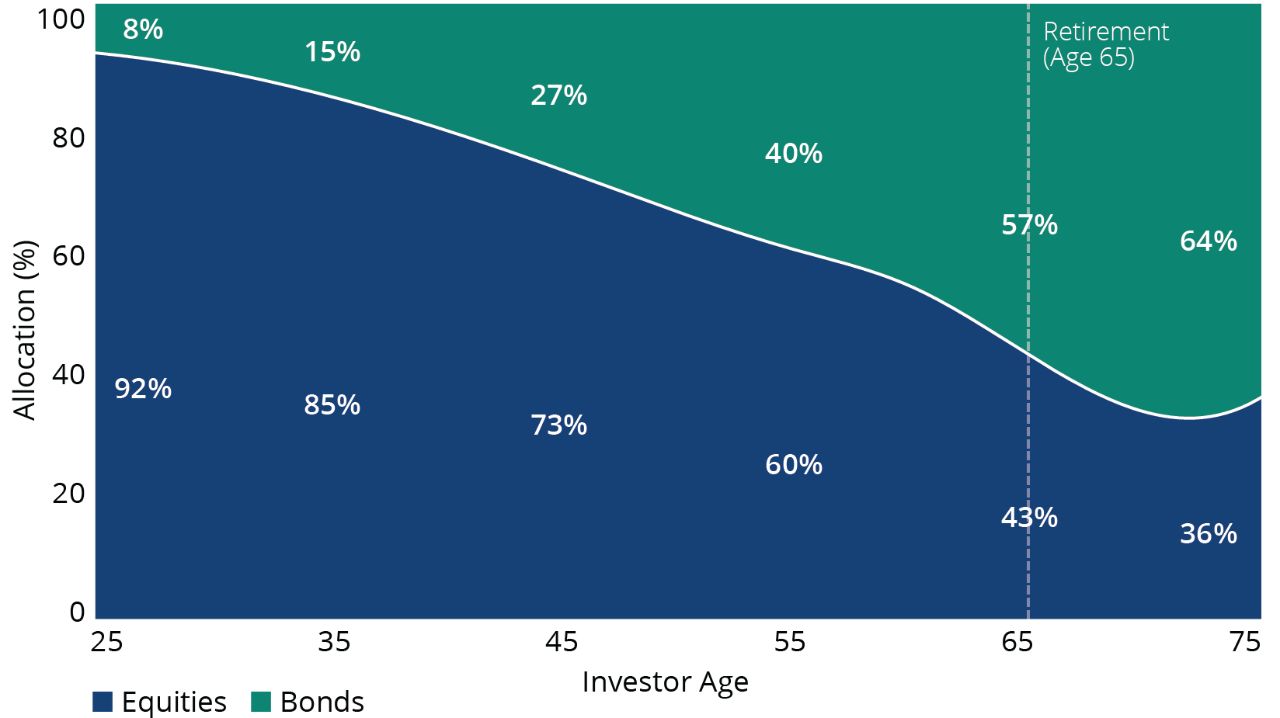

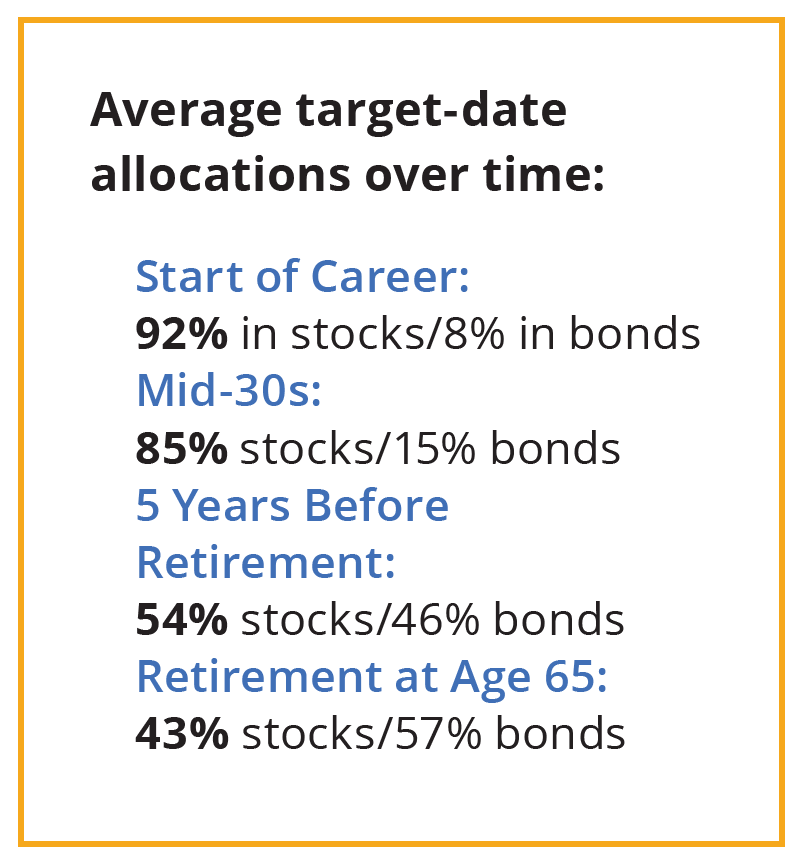

3. Retirement Default Options Are Quietly Converting Aging Into Bond Demand

Target-date funds and other lifecycle strategies typically follow glide paths that reduce equity exposure over time in favor of higher bond exposure. Morningstar’s analysis of target-date category averages illustrates this concept.

Glide Paths Are Designed to Reduce Risk as Investors Age

Sample glide path based on published target-date fund guidance. Allocations vary by provider and are shown here for illustration only. Not representative of any Hartford fund. Data Source: Morningstar, Target-Date Fund Landscape, 2025; Morningstar category averages as of December 31, 2024.

The key takeaway isn’t that every glide path should look the same, but rather that many retirement strategies have a built-in preference for bonds as investors age. This could create a durable demand for fixed income.

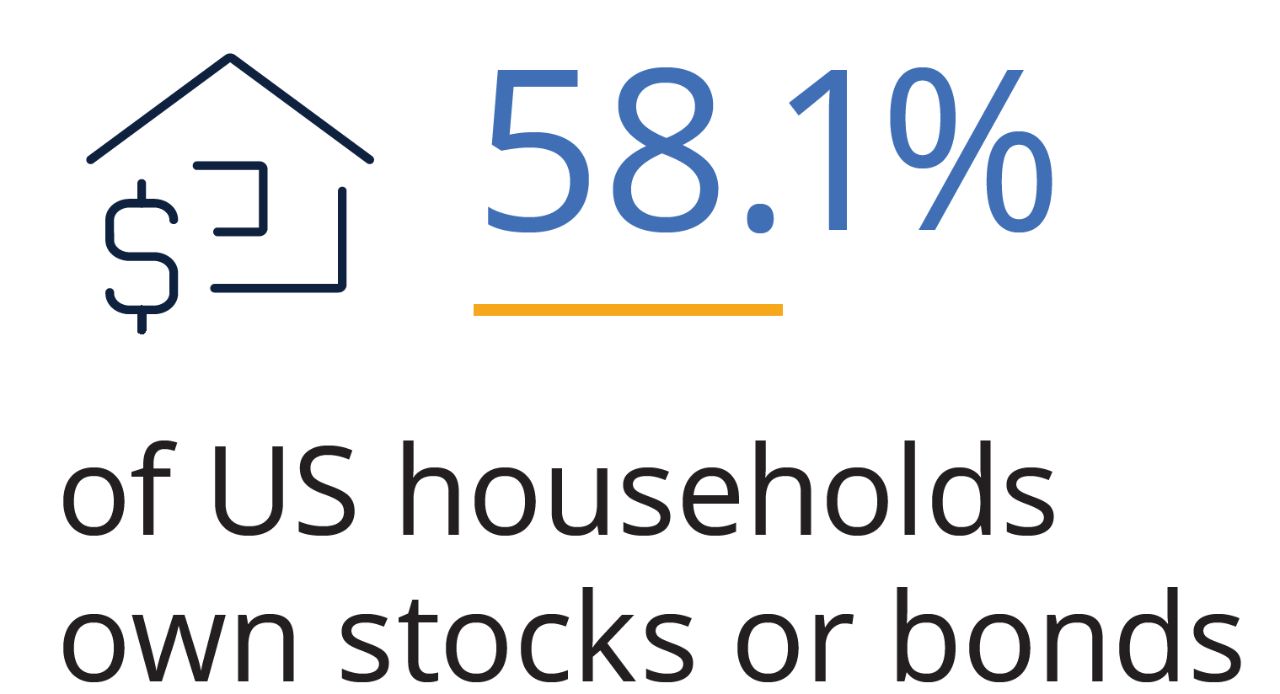

4. A Majority of US Households Are in the Market

Retirement-plan trends may seem to only affect a slice of investors, but the number of households that invest in the market suggests otherwise.

This breadth matters for two reasons: Broad market exposure across millions of households means retirement defaults carry enormous weight, and when participation is this widespread, the effects are magnified.

Data Source: SEC statistics based on the Survey of Consumer Finances (2022). Most recent data available.

What This Means for Portfolio Construction

The answer to these changes isn’t necessarily, “every investor should own more bonds.” Rather, these examples show why fixed-income demand can rise structurally when four forces converge: the retirement-age population grows, clients shift toward bonds as they approach retirement, retirement strategies automatically become more conservative as investors age, and broad market participation amplifies the effect.

Here are three practical ways to translate these trends into stronger client conversations:

The goal is to help clients build portfolios they can stick with as they age.

The Bottom Line

Fixed-income demand doesn’t rise only when yields look attractive or equities feel shaky. Sometimes it rises because needs are changing: The country is aging, and the retirement system is designed to shift portfolios toward bonds as investors age.

The demographic proof points are hard to ignore. The retirement-age population is projected to reach record highs, and the 2030s bring milestones that put that reality front and center. Meanwhile, target-date glide paths and broad market participation ensure those shifts reach a large share of households.

Financial professionals are well-positioned to connect these trends to client conversations by framing portfolio construction as a natural response to a client’s age. The goal isn’t to make a market call; it’s to help clients build portfolios they can stick with as they age.

To learn more about incorporating fixed income into your portfolio, talk to your financial professional.

Important Risks: Investing involves risk, including the possible loss of principal. • Fixed income security risks include credit, liquidity, call, duration, event and interest-rate risk. As interest rates rise, bond prices generally fall.

This information should not be considered investment advice or a recommendation to buy/sell any security. In addition, it does not take into account the specific investment objectives, tax and financial condition of any specific person. This information has been prepared from sources believed reliable but the accuracy and completeness of the information cannot be guaranteed. This material and/or its contents are current at the time of writing and are subject to change without notice.