After a rapid series of rate hikes in 2022 and 2023 aimed at cooling inflation, more conservative investments such as cash became increasingly attractive. Once inflation eased from its earlier highs, the Federal Reserve (Fed) shifted course, cutting rates through 2025 to support economic growth. With uncertainty now persisting around both inflation and growth, policy has moved into a less predictable cadence, settling into a more measured, pause-driven phase.

Pauses of this kind aren’t unusual. Since 1990, there have been 13 instances in which the Fed went 100 days or more between rate cuts, with the median stretch running about 330 days. That places the current environment within a pattern investors have seen before, even if this cycle reflects its own set of underlying conditions.

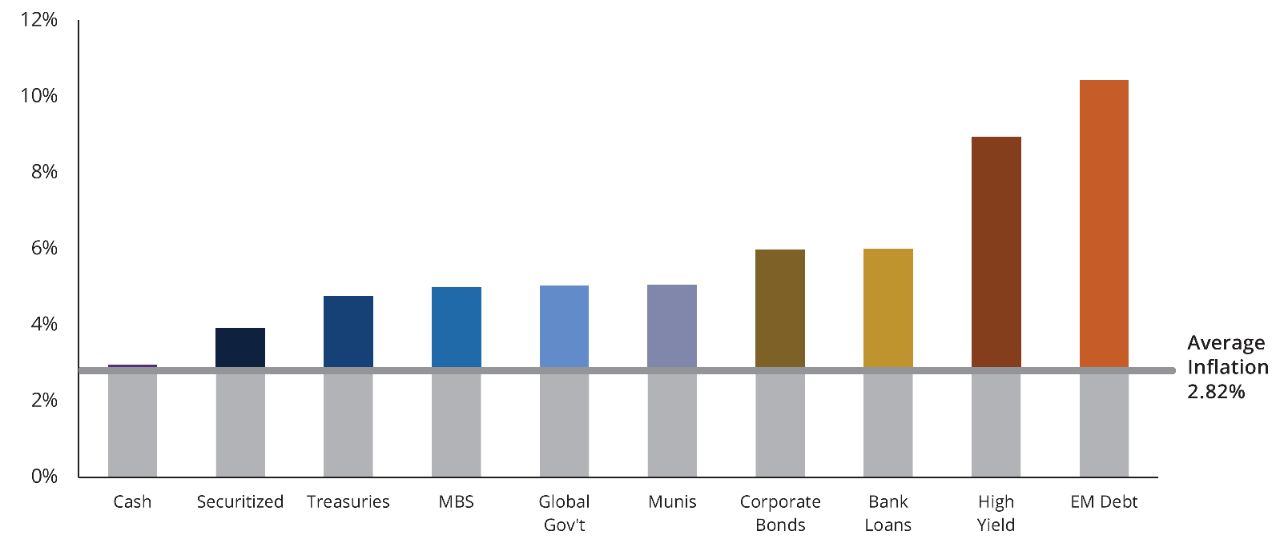

History has shown that the five years following a pause in rate cuts have produced a wide range of outcomes across fixed-income sectors (FIGURE 1), with most outpacing inflation over that period.

That dispersion of returns becomes even more apparent when viewed alongside cash. While previous rate hikes lifted short-term yields, cash has historically landed toward the lower end of outcomes once the Fed stops cutting. And real returns, or returns after taking inflation into account, make cash look even worse.