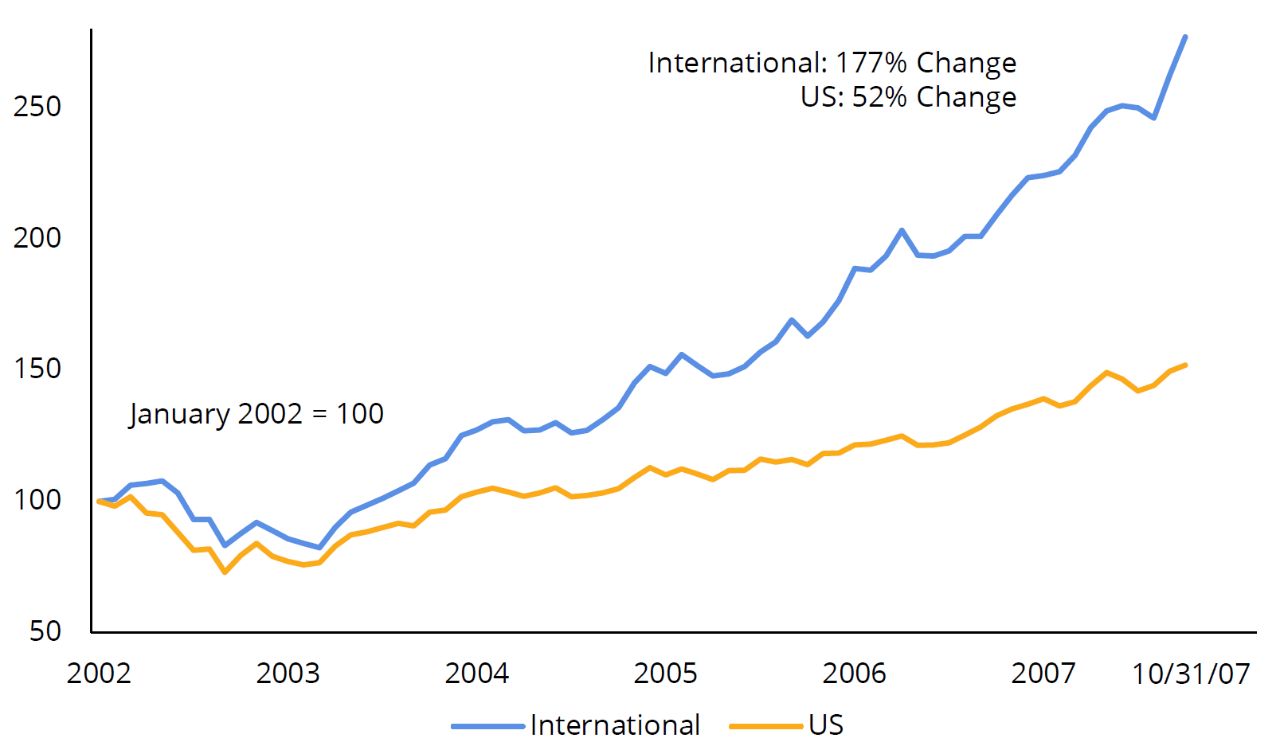

Historically, the case for an investment opportunity often appears most compelling near its peak, when strong growth, high profitability, and stellar past performance attract a widening pool of investors eager to buy into what seems like unstoppable momentum at any price.

Secular investment opportunities can be especially pernicious, as they frequently present themselves as a “new paradigm,” driven by innovation or structural change. And the longer leadership persists, the more the theme appears to be validated by its long-term performance. To gain perspective on today’s cycle, we revisit the defining secular growth stories of the past 75 years to explore whether familiar patterns are reemerging, or whether this time is truly different.

Late 1960s: The Rise of the “Nifty 50” as One-Decision Stocks

The Narrative: During the late 1960s, the 50 leading US large-cap stocks—including companies such as GE, Coca-Cola, and IBM—were experiencing rapid growth. By leveraging their scale and brand power, they expanded into new regions and business lines, consistently outpacing their competitors. Valuations climbed accordingly, with price-to-earnings1 multiples exceeding 30–40x in some cases. These levels were widely viewed as justified, supported by long track records of superior growth and profitability.

These dominant industry leaders were household names, characterized by wide competitive moats, strong balance sheets, and years of sustained stock-market outperformance. They came to be known as “one-decision stocks:” investments you bought once and never had to think about selling.

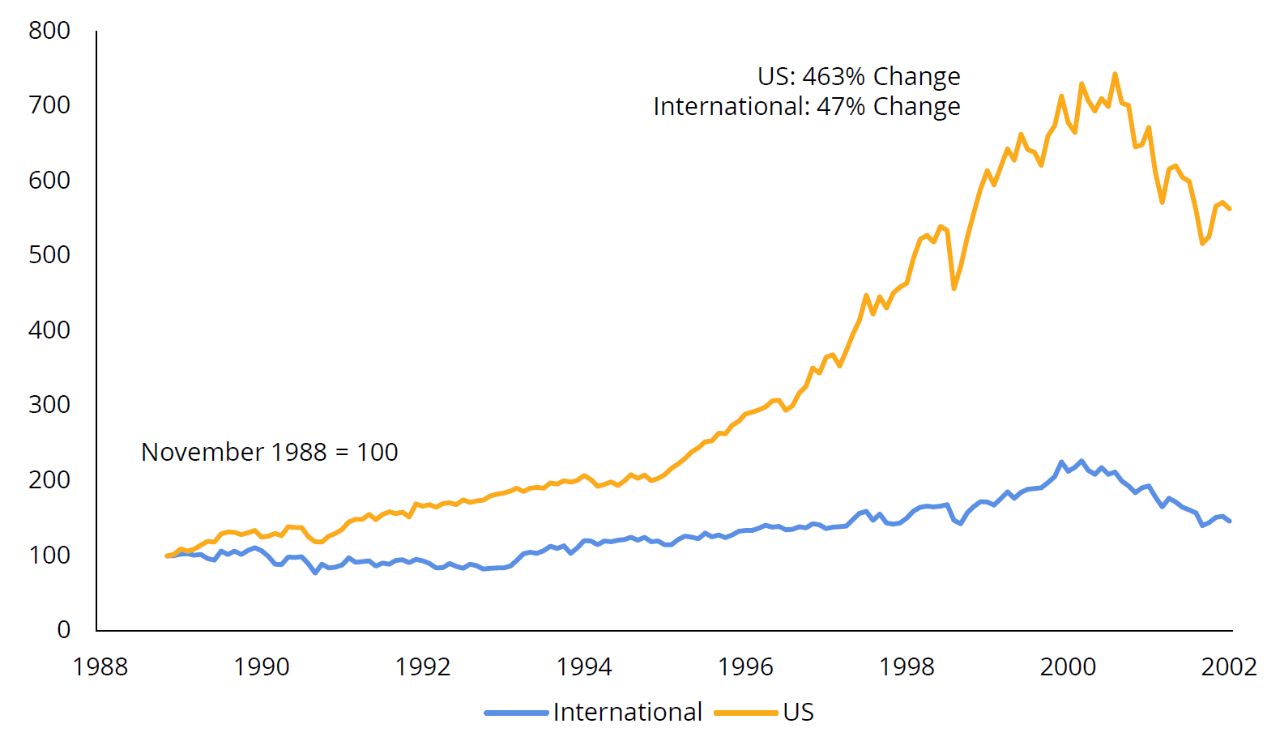

What Happened Next: As US earnings growth and market share came under pressure from the high interest rates and inflation of the early 1970s, the Nifty 50 stocks began to unravel. What followed was a two-decade period of underperformance for the US market relative to international stocks, exacerbated by rising foreign competition, the collapse of the savings and loan industry, and the 1987 stock-market crash.

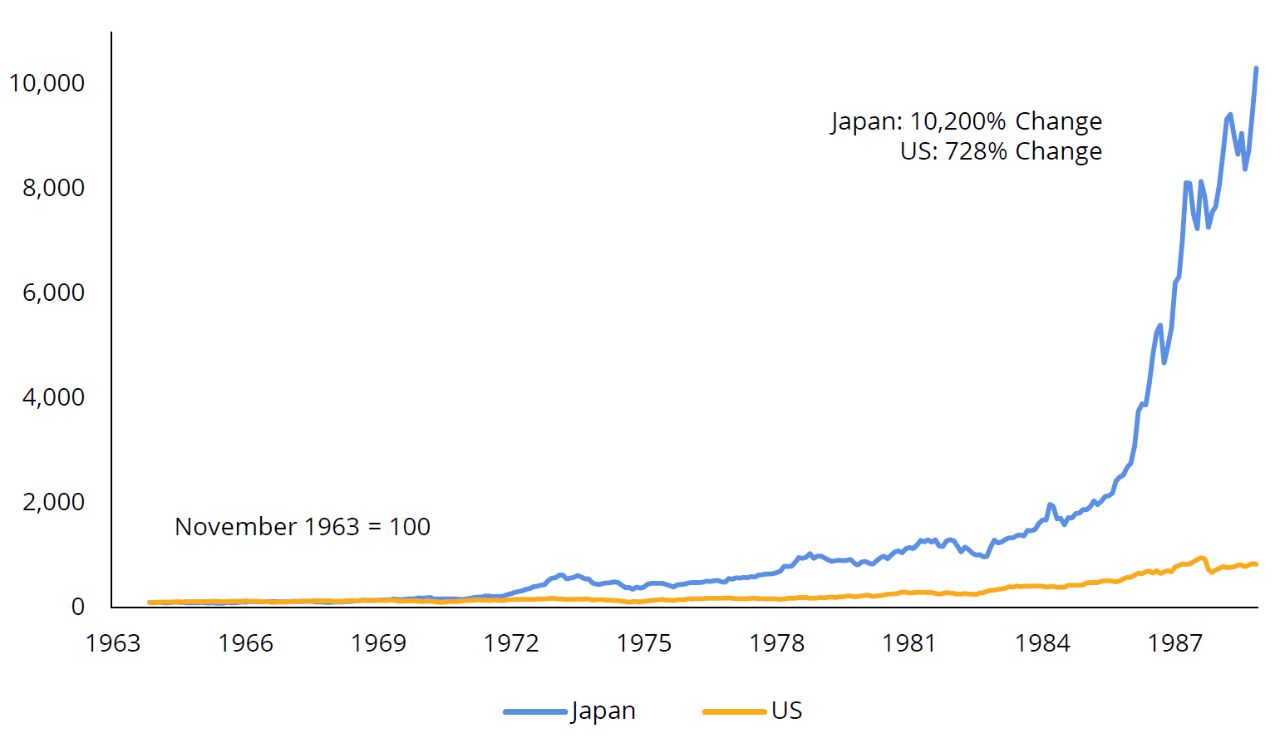

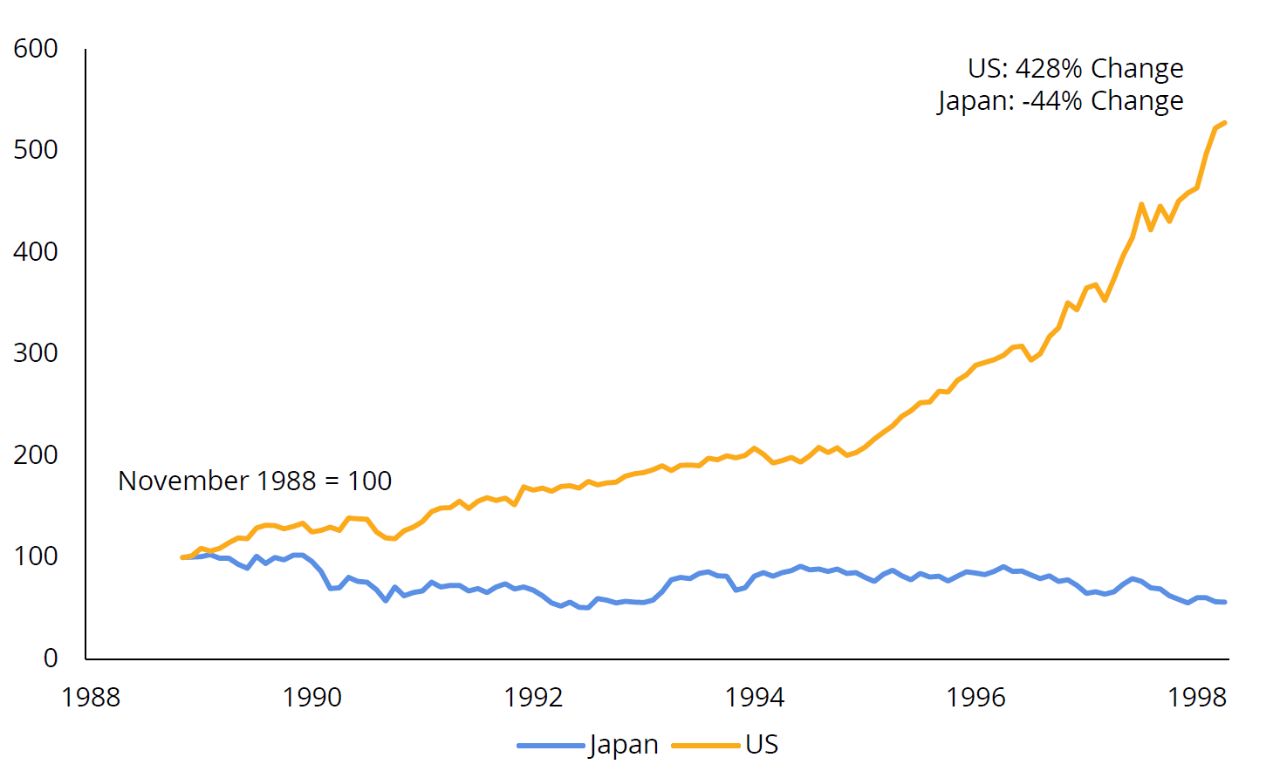

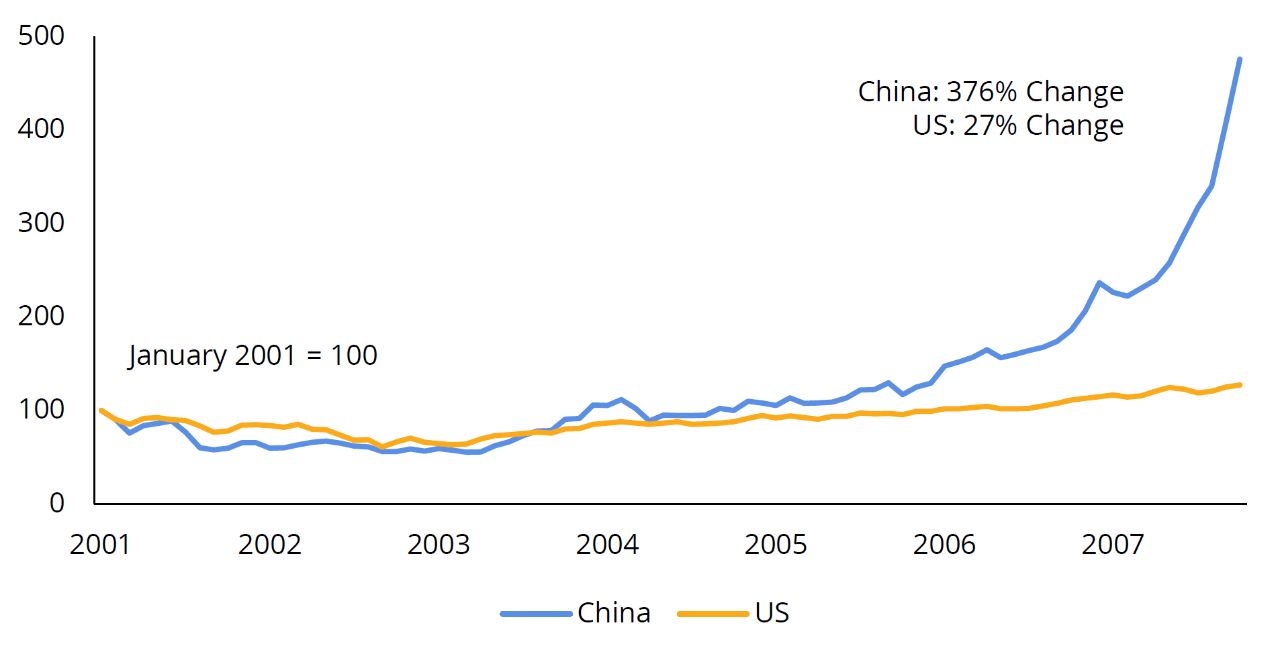

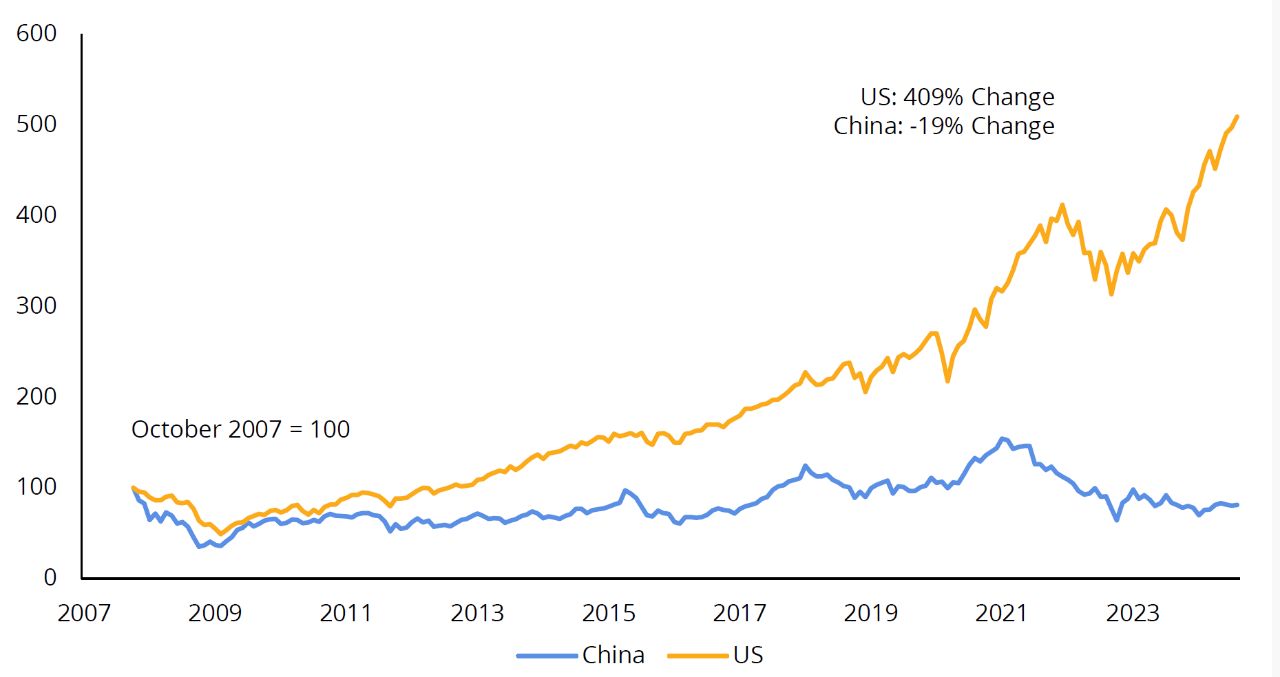

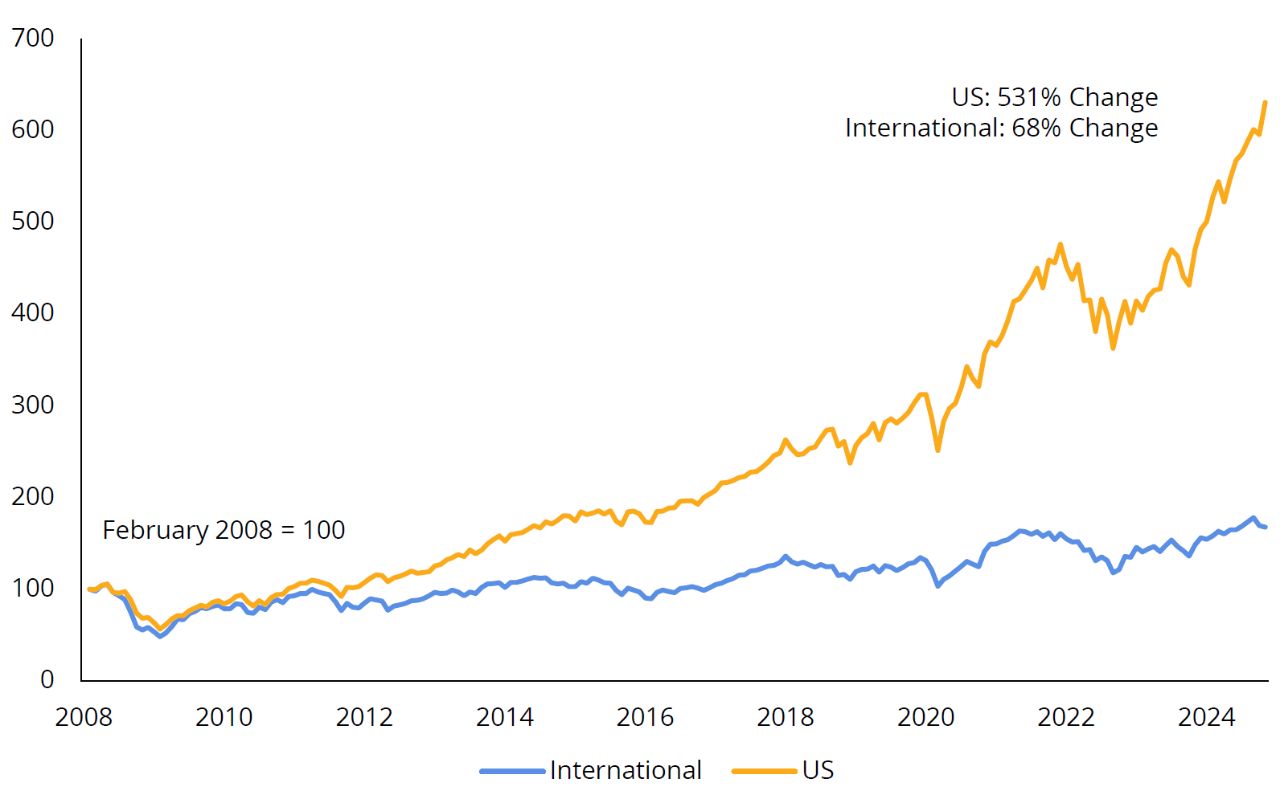

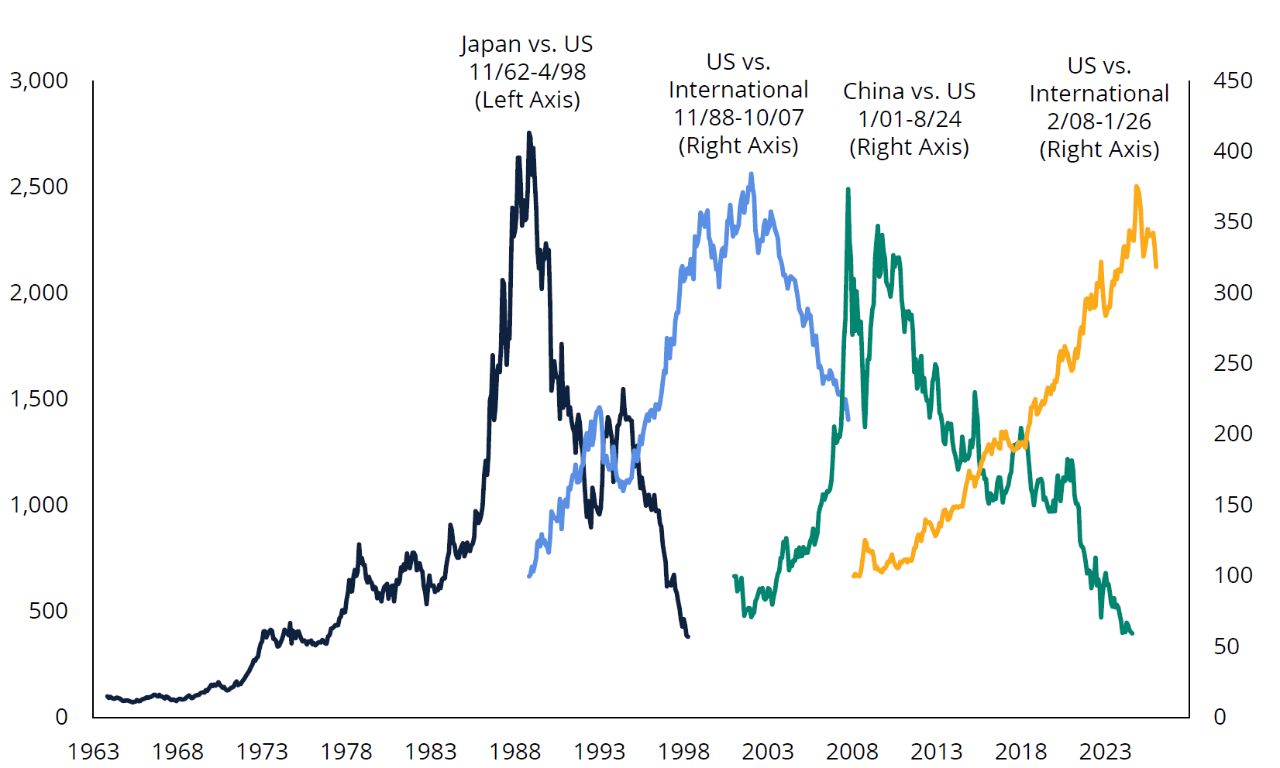

Late 1980s: Japan’s Rise to Market Dominance

The Narrative: During the late 1980s, Japan came to dominate technological innovation and manufacturing efficiency, capturing significant market share in critical industries such as automobiles (Toyota, Honda) and consumer electronics (Sony, Panasonic, Nintendo). Japan also became home to the world’s largest stock market, accounting for roughly 45% of the global stock market, as investors were drawn to its strong profit growth, technological advantages, and impressive returns (FIGURE 1).

At the peak of the boom, enthusiasm for all things Japanese ran so high that the land beneath Tokyo’s Imperial Palace was said to be worth more than all the real estate in the state of California.