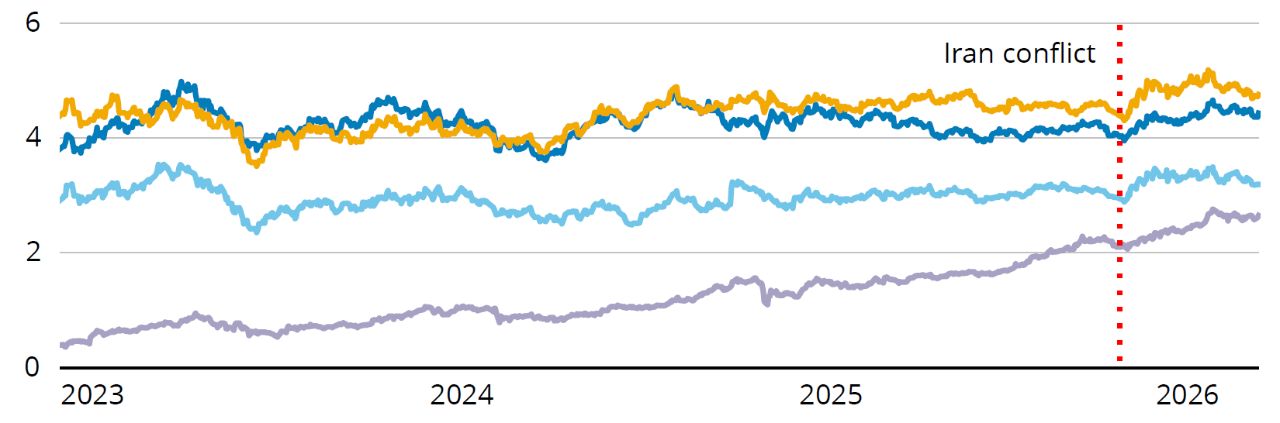

Indices used in FIGURE 1:

MSCI USA Index is a free float-adjusted market capitalization index that is designed to measure the performance of the large and mid cap segments of the US market.

MSCI Europe Index is a free-float adjusted market-capitalization-weighted index designed to measure the equity market performance of the developed markets in Europe.

MSCI Japan Index is a free-float adjusted market-capitalization index designed to measure large- and mid-cap Japanese equity market performance.

MSCI Emerging Markets Index a free float-adjusted market capitalization-weighted index that is designed to measure equity market performance in the global emerging markets. MSCI index performance is shown net of dividend withholding tax.

ICE BofA Global Government Index is a market value-weighted benchmark designed to track the performance of investment-grade sovereign debt publicly issued and denominated in the issuer’s domestic market.

ICE BofA US Corporate Index tracks the performance of U.S. dollar-denominated, investment-grade-rated corporate debt publicly issued in the U.S. domestic market.

ICE BofA Global High Yield Index tracks the performance of below-investment-grade corporate bonds denominated in US dollars, euros, British pounds, and Canadian dollars and issued in major global markets.

JPMorgan Emerging Markets Sovereign Index (EMBI Global Core) tracks total returns for traded external debt instruments in the emerging markets. It limits the weights of those index countries with larger debt stocks by only including specified portions of these countries’ eligible current face amounts of debt outstanding.

Dow Jones Commodity Index – Crude Oil tracks the performance of the crude oil commodities market by measuring the returns of WTI (West Texas Intermediate) crude oil futures contracts.

Dow Jones Commodity Index – Gold tracks the performance of the gold market using futures contracts.

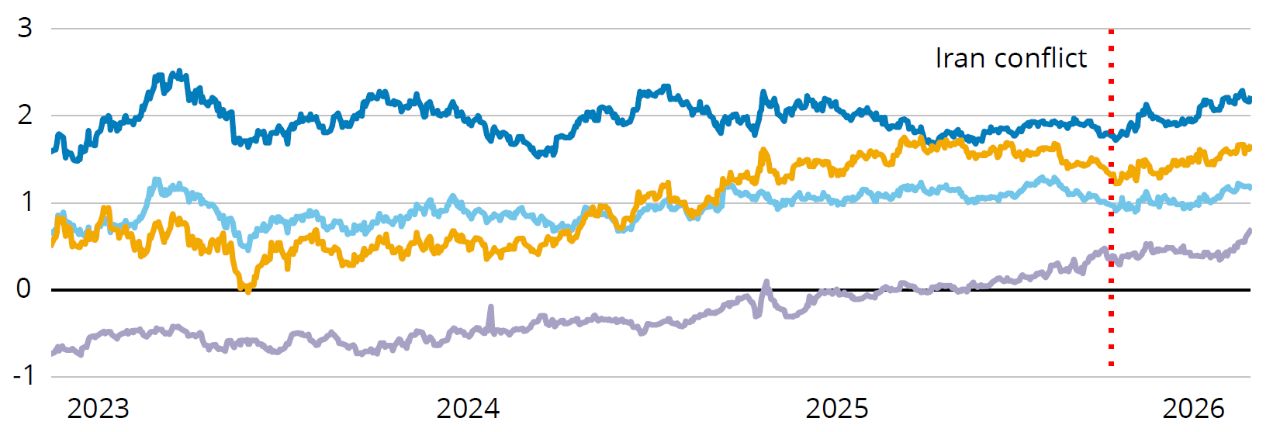

Indices used in FIGURE 2:

Nominal: US generic 10-year Treasury yield, Eurozone 10-year yield (Wellington composite of Germany [bund], France [OAT], and Italy [BTP]), UK generic 10-year government bond (gilt) yield, Japan generic 10-year government bond (JGB) yield; Real: US 10-year inflation-linked Treasury (TIPS) real yield (constant maturity), Eurozone 10-year real yield (Wellington composite of inflation-linked bonds from Germany, France, and Italy), UK 10-year inflation-linked gilt real yield, Japan 10-year inflation linked government bond real yield.

1 Earnings per share measures how much profit a company makes per share of common stock.

2 Stagflation is an economic cycle characterized by slow growth, inflation, and signs of labor market weakness.

3 Capital expenditures are funds used by a company to acquire, upgrade, and maintain physical assets such as property, plants, buildings, technology, or equipment. They are often used to undertake new projects or investments by a company.

4 Spreads are the difference in yields between two fixed-income securities with the same maturity but originating from different investment sectors.

5 Duration is a measure of the sensitivity of an investment’s price to nominal interest-rate movement.

6 The yield curve is a line that plots interest rates of bonds having equal credit quality but differing maturity dates; its slope is used to forecast the state of the economy and interest-rate changes.

7 Return on Equity is the average amount of net income returned as a percentage of shareholder’s equity over the past five years.

8 Carry is the difference between the yield on a longer-maturity bond and the cost of borrowing.

9 Correlation is a statistical measure of how two investments move in relation to each other. A correlation of 1.0 indicates the investments have historically moved in the same direction; a correlation of -1.0 means the investments have historically moved in opposite directions; and a correlation of 0 indicates no historical relationship in the movement of the investments.

10 Beta is a measure of risk that indicates the price sensitivity of a security or a portfolio relative to a specified market index.

Important Risks: Investing involves risk, including the possible loss of principal. • Foreign investments may be more volatile and less liquid than U.S. investments and are subject to the risk of currency fluctuations and adverse political, economic and regulatory developments. These risks may be greater, and include additional risks, for investments in emerging markets or if focused in a particular geographic region or country. • Fixed income security risks include credit, liquidity, call, duration, and interest-rate risk. As interest rates rise, bond prices generally fall. • Investments in high-yield (“junk”) bonds involve greater risk of price volatility, illiquidity, and default than higher-rated debt securities. • Investments in the commodities market may increase liquidity risk, volatility and risk of loss if adverse developments occur. • Investments in the technology sectors may go in and out of favor, which may cause underperformance.

The views expressed here are those of the authors and are based on available information and are subject to change without notice. This information should not be considered as investment advice or a recommendation to buy/sell any security. In addition, it does not take into account the specific investment objectives, tax and financial condition of any specific person. Portfolio positioning is at the discretion of the individual portfolio management teams; individual portfolio management teams and different fund sub-advisers may hold different views and may make different investment decisions for different clients or portfolios. This material and/or its contents are current as of the time of writing and may not be reproduced or distributed in whole or in part, for any purpose, without the express written consent of Wellington Management or Hartford Funds.