1 The yield curve is a line that plots interest rates of bonds having equal credit quality but differing maturity dates; its slope is used to forecast the state of the economy and interest-rate changes.

2 Spreads are the difference in yields between two fixed-income securities with the same maturity but originating from different investment sectors.

3 Risk assets refer to assets that have a significant degree of price volatility, such as equities, commodities, high-yield bonds, real estate, and currencies.

4 Duration is a measure of the sensitivity of an investment’s price to nominal interest-rate movement.

5 Carry is the difference between the yield on a longer-maturity bond and the cost of borrowing.

6 Beta is a measure of risk that indicates the price sensitivity of a security or a portfolio relative to a specified market index.

7 All‑in yield refers to the total yield available on a bond, reflecting both base interest rates as well as the additional income investors earn from taking on credit exposure.

8 Credit risk transfer securities (CRTs) are bonds that allow mortgage lenders to pass some of the risk of borrower defaults on to private investors in exchange for higher potential yields.

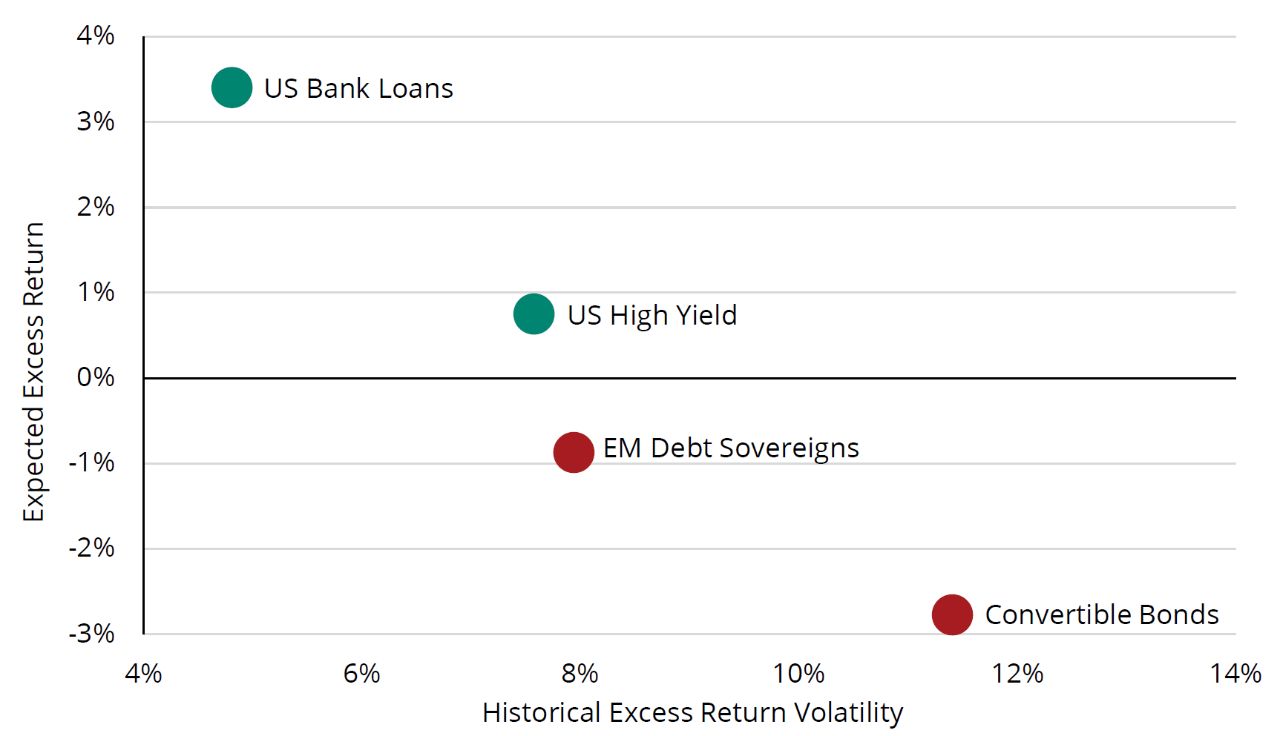

Representative Indices from Figure 1:

Convertible Bonds are represented by the Bloomberg US Bond Only Convertibles Index, which measures the performance of US convertible bonds, which offer the income characteristics of bonds with the potential to participate in stock market gains.

EM Debt Sovereigns are represented by the JP Morgan EMBI Global Diversified IG Index, which measures the performance of US dollar-denominated investment-grade bonds issued by emerging-market governments and government-related entities.

US Bank Loans are represented by the JP Morgan Leveraged Loan Index, which measures the performance of leveraged loans, which are loans made to below-investment-grade companies and typically offer floating interest rates.

US High Yield is represented by the Bloomberg US High Yield Index, which tracks the performance of US corporate bonds rated below investment grade, offering a broad measure of the high-yield, or “junk bond,” market.

Important Risks: Investing involves risk, including the possible loss of principal. Security prices fluctuate in value depending on general market and economic conditions and the prospects of individual companies. • Fixed income security risks include credit, liquidity, call, duration, event and interest-rate risk. As interest rates rise, bond prices generally fall. • Investments in high-yield (“junk”) bonds are considered speculative, involve heightened credit risk and greater risk of price volatility, illiquidity, and default than investment grade bonds. • Foreign investments, including foreign government debt, may be more volatile and less liquid than U.S. investments and are subject to the risk of currency fluctuations and adverse political, economic and regulatory developments. These risks may be greater, and include additional risks, for investments in emerging markets. • Derivatives are generally more volatile and sensitive to changes in market or economic conditions than other securities; their risks include currency, leverage, liquidity, index, pricing, valuation, and counterparty risk. • The risks associated with mortgage-related and asset-backed securities as well as collateralized loan obligations (CLOs) include credit, interest-rate, prepayment, liquidity, default and extension risk. • The purchase of securities in the To-Be-Announced (TBA) market can result in higher portfolio turnover, which could increase transaction costs and an investor’s tax liability. The risks associated with the TBA market include price and counterparty risk. • Restricted securities may be more difficult to sell and price than other securities. • Loans can be difficult to value and less liquid than other types of debt instruments; they are also subject to nonpayment, collateral, bankruptcy, default, extension, prepayment and insolvency risks. • Obligations of U.S. Government agencies are supported by varying degrees of credit but are generally not backed by the full faith and credit of the U.S. Government. • The portfolio managers may allocate a portion of the Fund’s assets to specialist portfolio managers, which may not work as intended.

Additional risks for Hartford Strategic Income ETF: The market price of the Fund’s shares will fluctuate in response to changes in the Fund’s net asset value, intraday value of the Fund’s holdings, and the supply and demand for shares on the exchange. • The Fund is actively managed and does not seek to replicate the performance of a specified index. • The Fund may effect creations and redemptions partly or wholly for cash, rather than in-kind, which may make the Fund less tax-efficient and incur more fees than an ETF that primarily or wholly effects creations and redemptions in-kind. • The Fund may have high portfolio turnover, which could increase its transaction costs and an investor’s tax liability.

Diversification does not ensure a profit or protect against a loss in declining market

The views expressed herein are those of Wellington Management, are for informational purposes only, and are subject to change based on prevailing market, economic, and other conditions. The views expressed may not reflect the opinions of Hartford Funds or any other sub-adviser to our funds. They should not be construed as research or investment advice nor should they be considered an offer or solicitation to buy or sell any security. This information is current at the time of writing and may not be reproduced or distributed in whole or in part, for any purpose, without the express written consent of Wellington Management or Hartford Funds.