We entered 2026 with sharp price shifts in software and AI-related equities, as advances in enterprise AI tools, including Anthropic’s Claude, pressured software valuations and heightened concerns that AI could displace parts of the labor force. Market sentiment was further unsettled by prominent corporate announcements linking workforce reductions to gains in AI-driven efficiency.

Our view remains that AI could be disinflationary over the medium to long term, largely due to its potential to drive productivity gains. Over the past 12 months, the labor market has been characterized by both low hiring and low firing. While this partly reflects supply-side constraints, such as minimal population growth, we also see signs of softening labor demand, particularly among large-cap companies.

A consistent message from management teams has been the push to do “more with the same”—in other words, to grow earnings without materially increasing headcount. In our view, this reflects productivity gains and points to a weaker medium-term outlook for labor demand. With its focus on supporting stable employment, we believe the Federal Reserve (Fed) is watching this dynamic closely.

Although the labor market has stabilized and private-sector activity is showing some improvement, we don’t view the current backdrop as especially strong. We also expect a meaningful share of future productivity gains to accrue more to capital than to labor.

Historically, higher productivity has supported real wage growth, as technology increased output per worker and encouraged additional hiring. If AI evolves in a way that reduces the need for incremental labor, that relationship may weaken. In our view, the path of AI adoption will be one of the defining macro and micro investment themes for the foreseeable future. On balance, we believe it points to lower inflation and a more favorable growth-inflation mix over time—an environment that can be constructive for both stocks and bonds.

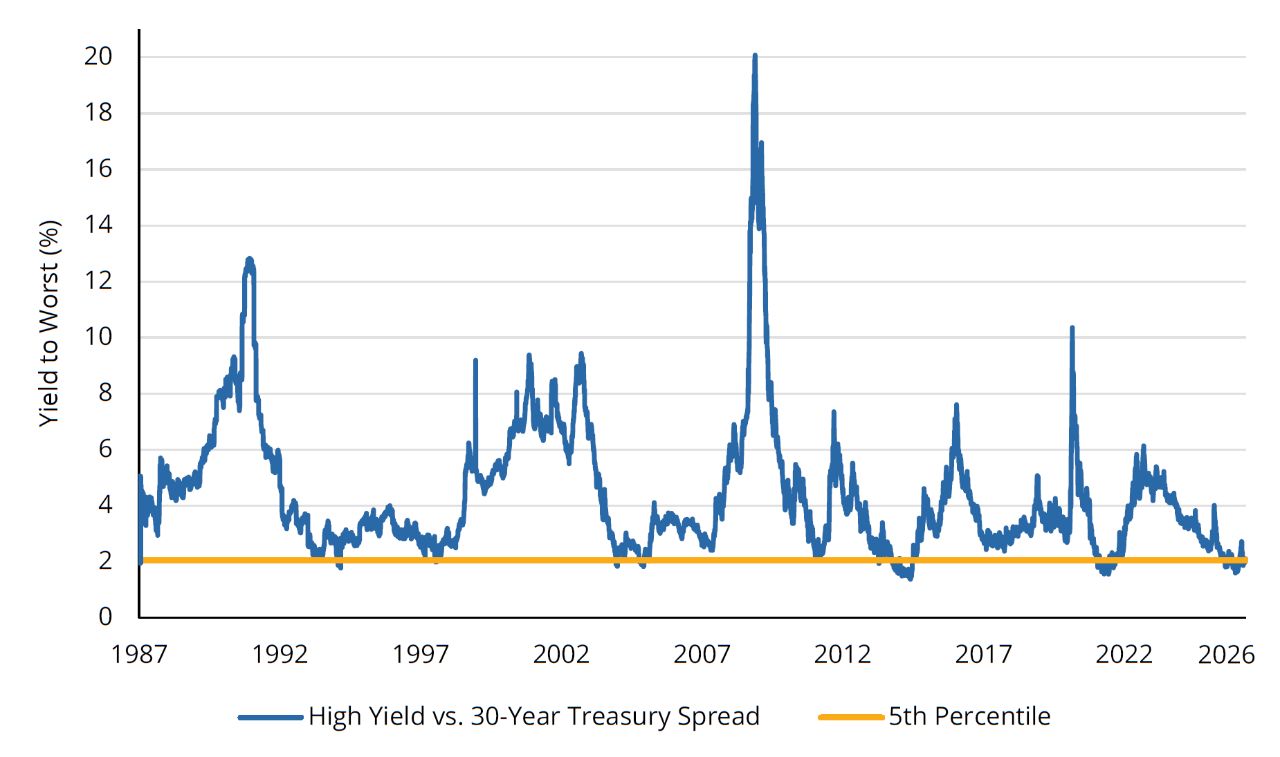

Over the past six months, the backdrop has been shaped by a stabilizing labor market, inflation that remains above the Fed’s 2% target, strong fiscal support, and AI-related capital spending that has surprised to the upside. In some cases, that spending has also added to near-term inflation due to supply constraints, while the Iran war has introduced an oil-related supply shock. Together, these forces help explain the rise in bond yields. Looking ahead, however, the backdrop may begin to shift:

- Fiscal impulse nearing a peak – We believe fiscal impulse (how government spending and taxes are shaping growth) is close to its peak for this cycle. If additional spending is pursued, the risk of a bond-market backlash rises meaningfully. Our base case is that a reconciliation bill is unlikely to pass before the midterms. If it does, we would likely view any resulting rise in yields as an attractive opportunity to add to bonds. Historically, yields have often peaked in the summer heading into midterm elections, and we would expect a more constrained fiscal backdrop if Republicans lose seats.

- Limited population growth – Zero population growth remains an important long-term headwind to economic growth, and we believe the market is underappreciating that constraint.

- Housing as a disinflationary force – The housing market remains unaffordable and appears to be gradually cooling, which we see as a meaningful source of disinflation.

- AI and the inflation mix – Whether AI ultimately reduces employment remains uncertain, but we do see it as a potentially powerful disinflationary force. In that environment, growth could remain reasonable while the balance between growth and inflation improves.

- AI capex growth moderating – In the AI capex cycle, we expect the pace of growth to slow in the coming months. From current levels, it’s difficult to envision a meaningful reacceleration, though we remain open to that possibility.

- Oil shock scenarios – We see two broad paths in the Iran conflict. A resolution that restores oil flows would likely push prices lower, though not necessarily back to prior levels given infrastructure damage. A more prolonged disruption could leave Europe and parts of Asia facing physical supply shortages. In either case, we believe lower bond yields are ultimately more likely.