With the technology-focused Magnificent Seven1 stocks accounting for about 25% of the value of the S&P 500 Index,2 investors are looking for any signs that market breadth will improve and make room for other sectors and styles to outperform. I think one interesting space to explore is US small-cap stocks.

While small caps are more volatile than large-cap stocks, I see several reasons investors may want to consider an allocation to US small caps in a diversified portfolio:

- Economic growth expectations for the US are stronger than in Europe, the UK, and Japan, which could benefit domestically oriented small-cap stocks.

Last year, the consensus view was that a recession was on the way. But with consumer spending remaining healthy, inflation moderating, and interest-rate cuts on the horizon, the economy might actually be accelerating. And, given their greater economic sensitivity, this could actually be an environment in which small caps excel.

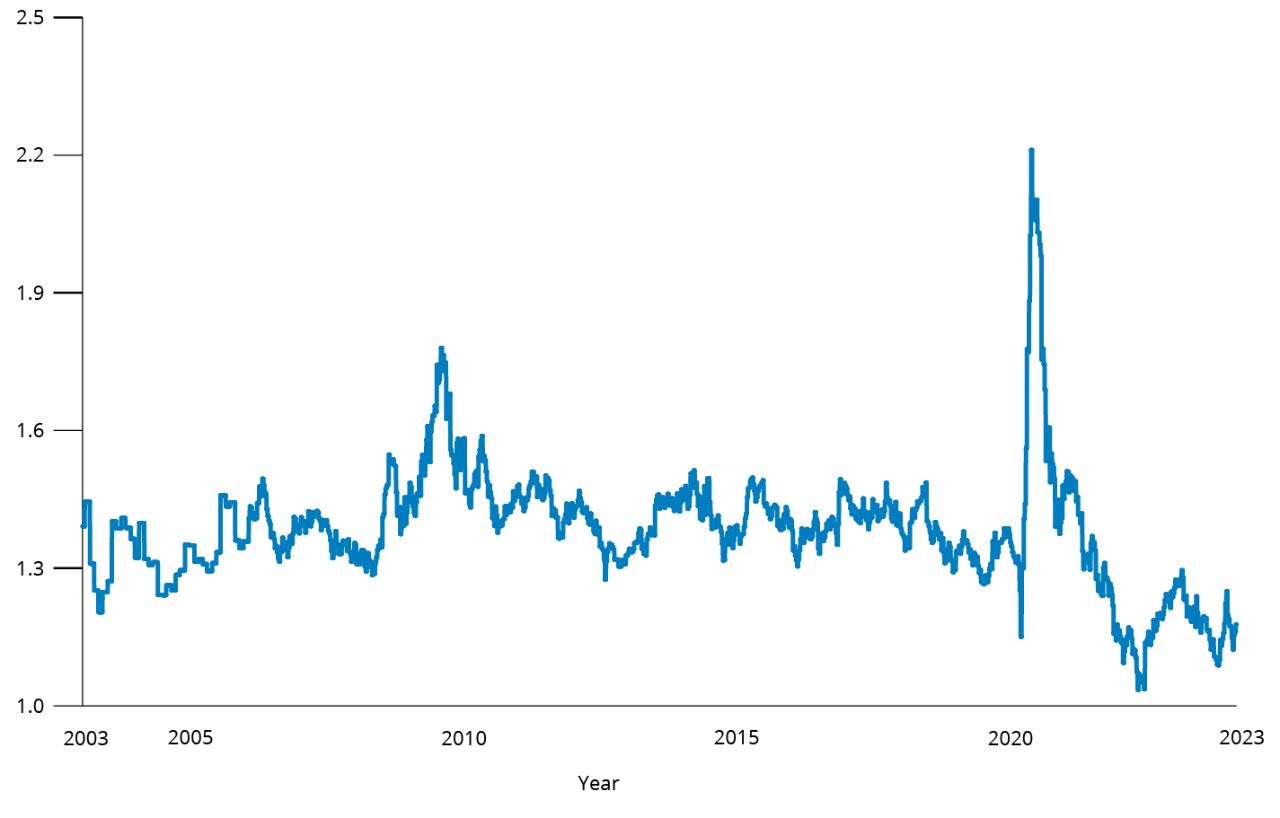

- Small-cap valuations look attractive relative to large caps.

Small caps have underperformed large caps over the past 11 years, yet we find that, historically, the cycle of large-cap outperformance over small caps has averaged about 10 years and then reversed. With the small-cap forward price/earnings (P/E) ratio3 at one of its lowest levels in recent years relative to the large-cap forward P/E ratio (FIGURE 1), a switch to small-cap outperformance may be due if the long-term pattern holds.