With US 10-year yields close to 5% and the end of the year approaching, it may be time to consider whether to move from cash to bonds. In my August commentary, I showed the potential benefit of bond investments even when it’s uncertain how long the Federal Reserve (Fed) will remain in interest-rate-hiking mode. Today, there’s a bit more clarity on the Fed, with markets expecting the central bank to remain on hold and begin cutting rates by mid-2024 as of this writing. Still, we don’t know for sure that the Fed is done. So I’ve taken a fresh look at why it may be better to invest in bonds before the last rate hike rather than after it.

What We Can Learn from Past Rate Hiking Cycles

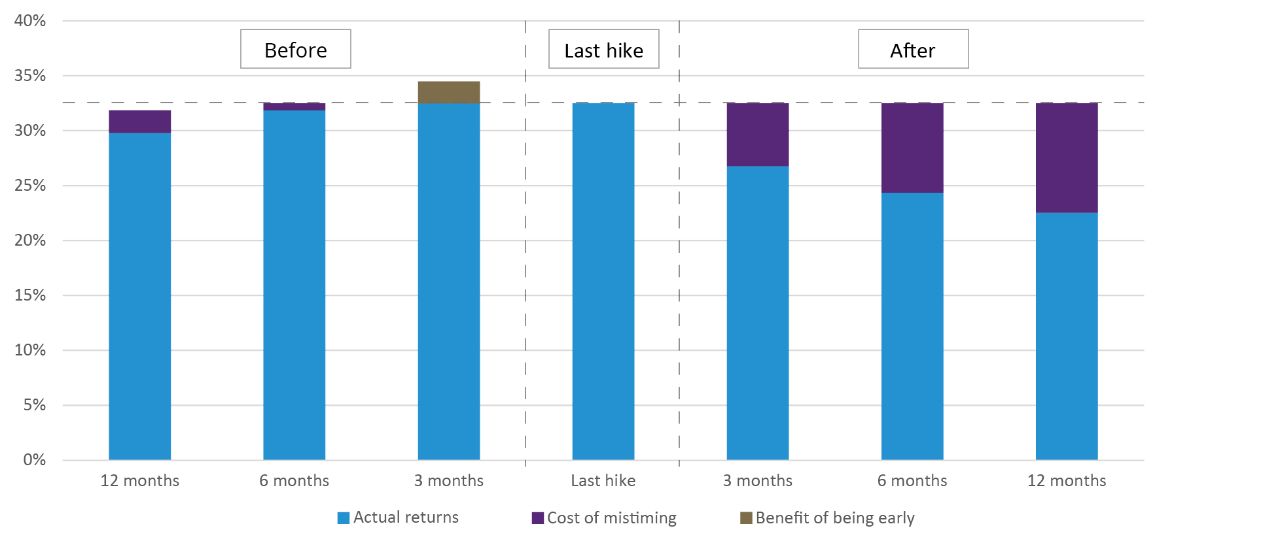

Using data from the past six Fed rate-hiking cycles, FIGURE 1 shows the average three-year total-return advantage of being in the Bloomberg US Aggregate Bond Index1 if an investor was three, six, or 12 months early relative to the last hike (left side of the chart), and three, six, or 12 months late relative to the last hike (right side of the chart). The purple shaded areas represent the lost total return compared to timing the last hike perfectly, shown in the middle bar, or the “cost of mistiming” the last hike. The gold shaded area is the additional total return earned compared to timing the last hike perfectly.