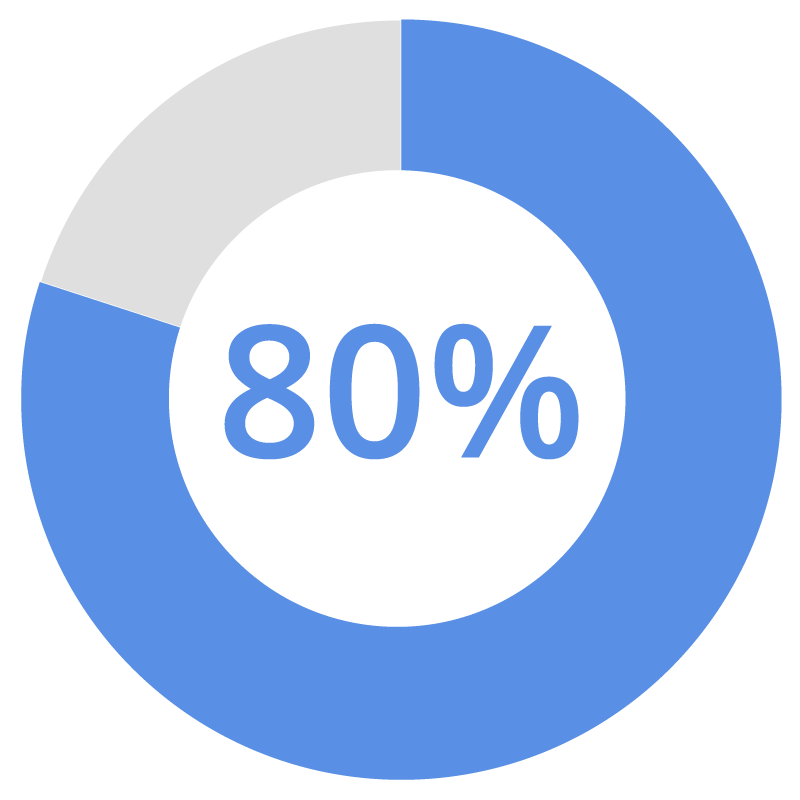

80% of clients would change financial professionals if theirs couldn’t help them maximize their Social Security benefits1

Many financial professionals say they’re reluctant to initiate Social Security conversations. They think the topic is too complicated and don’t want to risk being asked a question they can’t answer. Unfortunately, those financial professionals could not only be missing chances to help their clients but also asset-gathering opportunities. Here’s the good news: Providing valuable guidance to clients doesn’t require you to be a Social Security expert. The following three-question process can help increase clients’ confidence in their retirement-income plan and help you consolidate assets that reside outside of your firm.

First, “What Are You Expecting From Social Security?”

One of the most important things you can do for your clients is show them how to find out the amount of Social Security retirement income they’re entitled to receive. Why? Among those recently surveyed, more 36% aren’t sure how much their monthly benefit will be.1 Worse yet, there’s also a tendency for workers to overestimate their monthly Social Security benefits. Thirty-six percent of retirees said the Social Security income they’re receiving is substantially lower than what they expected.2

To find out their projected benefit, clients can view their Social Security statement online at ssa.gov. They can see their benefit estimates based on various ages at which they might file—before full retirement age (FRA), filing at FRA, and delayed filing—and the difference can be substantial. To access their statement, clients need to have a “my Social Security” account. If they don’t have an account, they can easily create one. You may have savvy clients who’ve done their homework and know what their monthly benefit will be. Either way, it can’t hurt to double-check. While they’re at it, urge clients to confirm the accuracy of their personal information, including their earnings history.

Once you have your client’s projected Social Security income, move on to the next question.