A Changing Market Backdrop

For years, investors faced a world defined by low inflation, low interest rates, and rising stock prices. That environment began to shift in 2022 as inflation surged and central banks raised rates aggressively. Since then, inflation has moderated, but it hasn’t fully returned to pre-pandemic norms.

Today’s market reflects a balance of competing forces:

- Inflation is lower than its peak, but still above long-term targets.

- Economic growth has remained resilient, supported by consumer spending and fiscal policy.

- Interest rates remain higher, changing the relative appeal of stocks, bonds, and cash.

Rather than signaling a return to the old regime, these conditions suggest a more complex environment—one in which both risks and opportunities exist across asset classes.

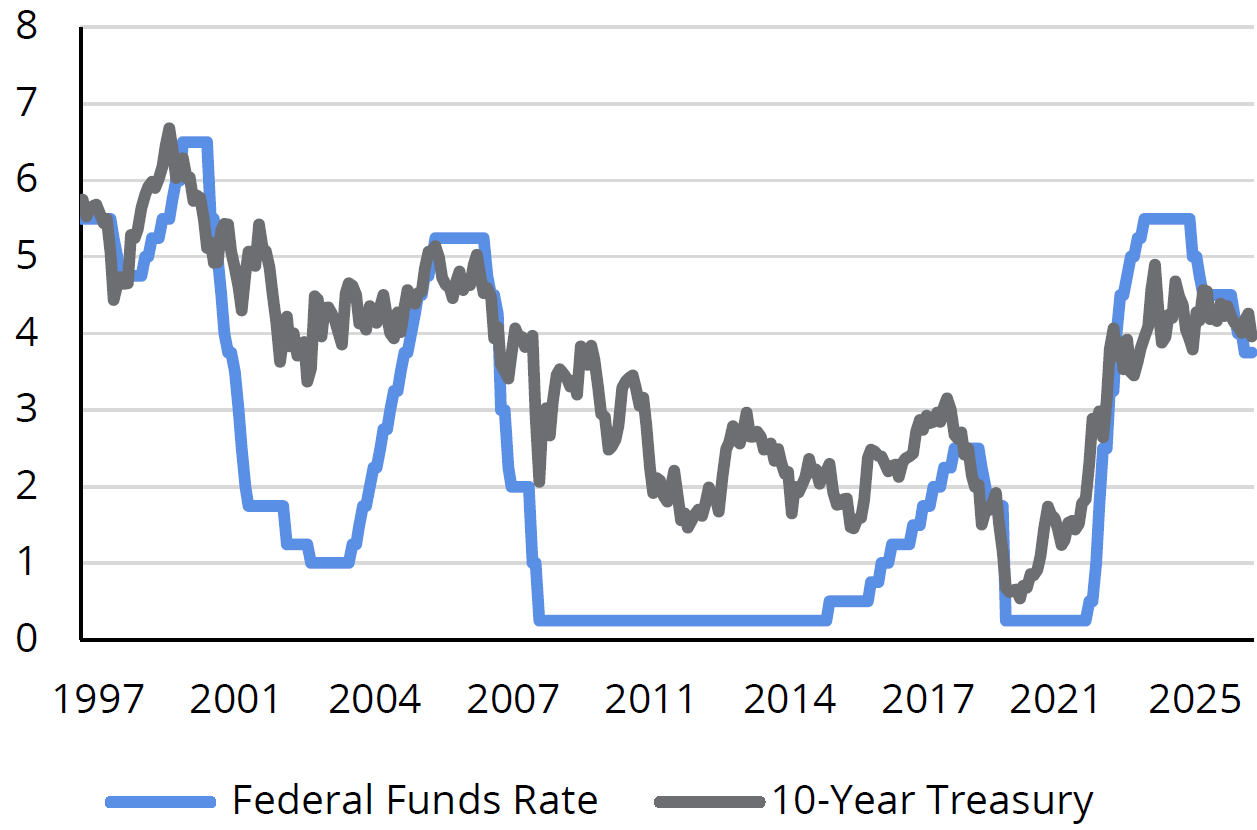

Why Fixed Income Looks Different Now

For years, bonds offered limited income and did little to hedge against inflation. But bond investments now look more attractive once again.

Several factors are driving renewed interest in fixed income: Higher yields mean bonds may pay investors more than they did for much of the past decade, restoring income potential to fixed-income allocations.

At the same time, bonds may once again help offset stock-market volatility, particularly if economic growth slows. And with the gap between stock valuations and bond yields having narrowed, the trade-offs between risk and return across asset classes are now more balanced than they‘ve been in years.

While bonds still have their risks, today’s starting yields provide a cushion that was largely absent in the past (FIGURE 1).