Pre-Sales Support

Mutual Funds and ETFs - 800-456-7526

Monday-Thursday: 8:00 a.m. – 6:00 p.m. ET

Friday: 8:00 a.m. – 5:00 p.m. ET

Post-Sales and Website Support

888-843-7824

Monday-Friday: 9:00 a.m. - 6:00 p.m. ET

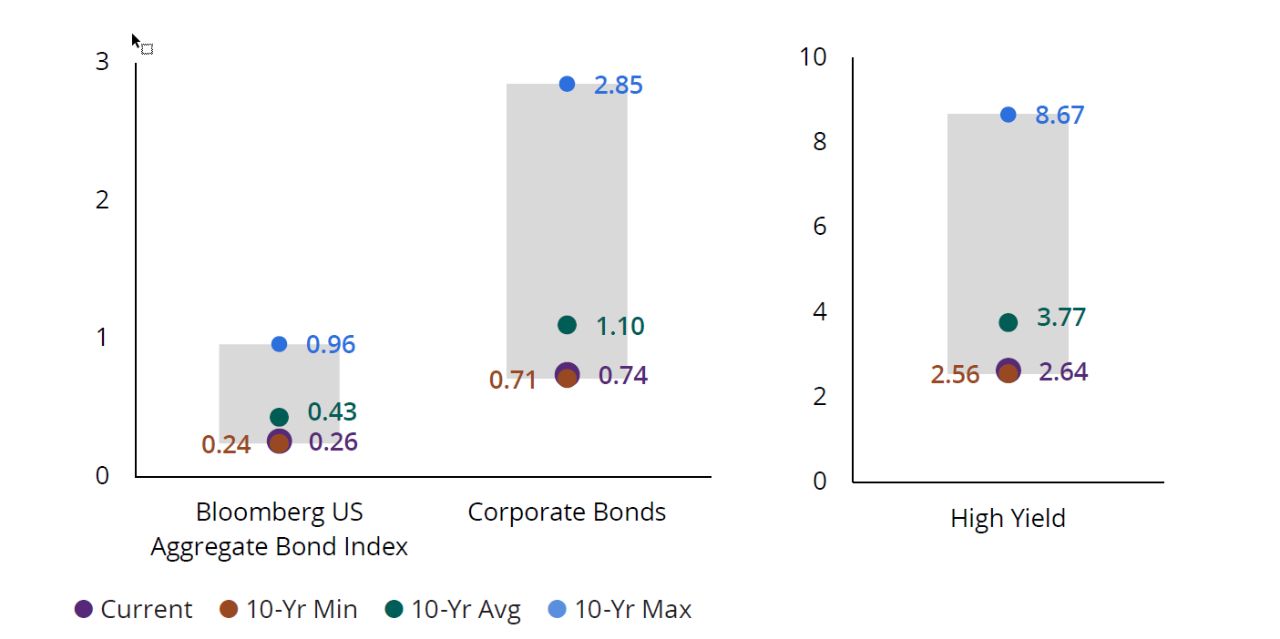

In today’s bond market, investors are being paid less for taking on risk—at a time when uncertainty can resurface quickly. One of the clearest signals of this dynamic is credit spreads, which have reached their tightest levels in almost 20 years.

Credit spreads (the difference in yield between a bond with credit risk and a risk-free Treasury of the same maturity) serve as the market’s real-time price tag on credit risk. Investors expect this additional yield to compensate for potential challenges, including changing cash flows, evolving market cycles, or periods of limited liquidity in risk assets.

Because spreads incorporate both fundamentals and sentiment, they provide a simple way to understand how much risk investors are willing to assume.

FIGURE 1

Spreads Are Near Historically Tight Levels

10-Year Yield (%) Spread Range

As of 6/30/26. Past performance does not guarantee future results. Indices are unmanaged and not available for direct investment. Corporate Bonds and High Yield represented by the Bloomberg US Corporate Bond Index and the Bloomberg US Corporate High Yield Bond Index, respectively. Please see below for index definitions. Data Sources: Bloomberg and Hartford Funds, 7/26.

Potential Advantages of Actively Managed Strategies

Beyond describing market conditions, credit spreads help frame the opportunity set. Narrow spreads reflect market confidence and healthy liquidity, as well as positive expectations for corporate balance sheets and the broader economy. Wider spreads, by contrast, can signal market uncertainty and elevated credit risk.

In a narrow-spread environment, investors receive less compensation for taking on additional risk. As a result, they may be tempted to take on more credit risk in an effort to generate just a little more yield. This could lead to portfolio volatility if spreads suddenly widen, but wider spreads can also create opportunities to buy securities at more attractive prices. Active managers can offer a disciplined approach to investing as these conditions evolve over time.

In addition, the size and complexity of bond markets can result in many nuances among sectors and security types. Even with tighter spreads across the broader bond market, there are still attractive opportunities within certain sectors where spreads meaningfully differ from the index average. And bond opportunities can exist outside of traditional bond indices, offering compelling returns and income opportunities that may not be available to a passive investor.

Active, flexible fixed-income strategies can access those opportunities by applying research, selectivity, and risk discipline across a complex and evolving bond market.

And in an environment where compensation for risk is limited and where market conditions can change quickly, that discipline can make a meaningful difference.

To learn more about managing fixed-income risk, please talk to your financial professional.

Bloomberg US Aggregate Bond Index is composed of securities that covers the US investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

Bloomberg US Corporate Bond Index covers all publicly issued, fixed rate, nonconvertible, investment grade debt.

Bloomberg US Corporate High-Yield Bond Index is an unmanaged broad-based market-value-weighted index that tracks the total return performance of non-investment grade, fixed-rate, publicly placed, dollar denominated and nonconvertible debt registered with the Securities and Exchange Commission.

Important Risks: Investing involves risk, including the possible loss of principal. • Fixed income security risks include credit, liquidity, call, duration, and interest-rate risk. As interest rates rise, bond prices generally fall. • Investments in high-yield (“junk”) bonds are considered speculative, involve heightened credit risk and greater risk of price volatility, illiquidity, and default than investment grade bonds.

This information should not be considered investment advice or a recommendation to buy/sell any security. In addition, it does not take into account the specific investment objectives, tax and financial condition of any specific person. This information has been prepared from sources believed reliable, but the accuracy and completeness of the information cannot be guaranteed. This material and/or its contents are current at the time of writing and are subject to change without notice.