If you’ve been working most of your life and have arrived at your sixth decade, congratulations: You’re entitled to collect what could potentially be thousands of dollars in annual Social Security benefits. And if you’re married, you may be eligible for something more: a spousal benefit that can potentially provide a meaningful boost for spouses whose own work history may have produced a smaller Social Security benefit. For couples seeking to maximize retirement income, spousal benefits may be worth a closer look.

But the ins and outs of spousal benefits are complicated and frequently misunderstood. That’s too bad, because a spousal benefit, for those that qualify, can potentially provide as much as half of a higher-earning spouse’s full-retirement-age (FRA) benefit.

Your Mileage May Vary

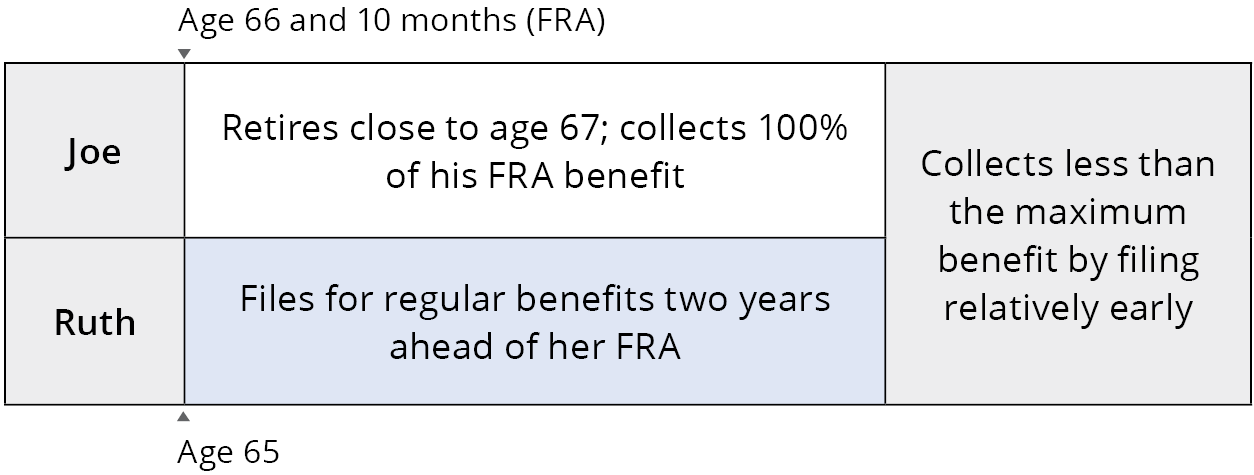

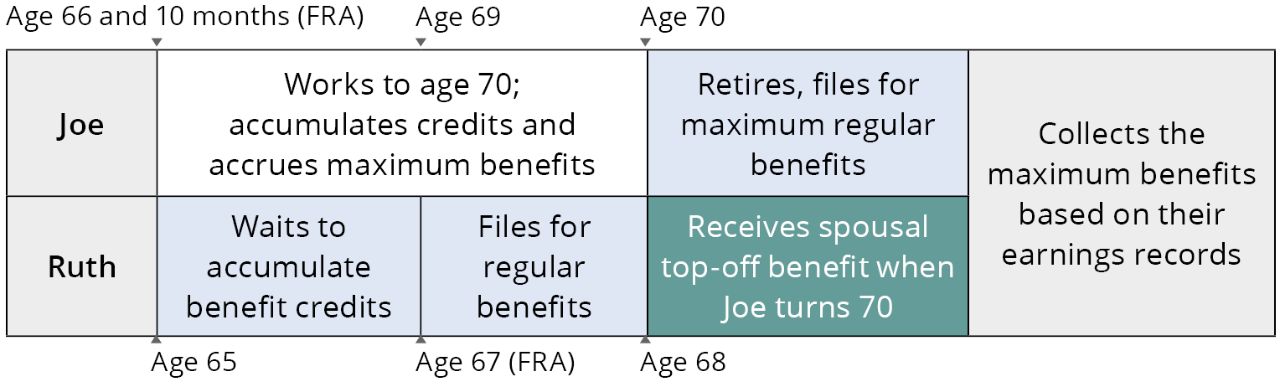

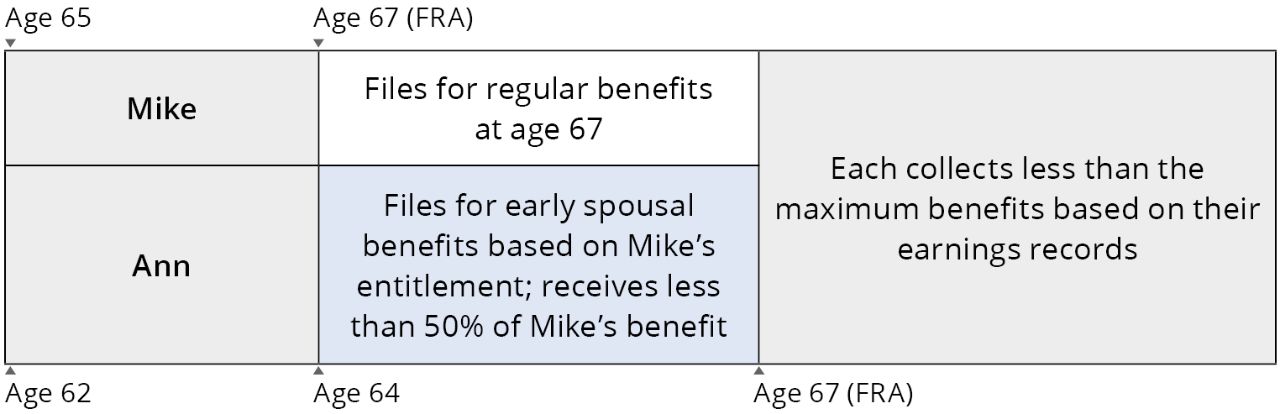

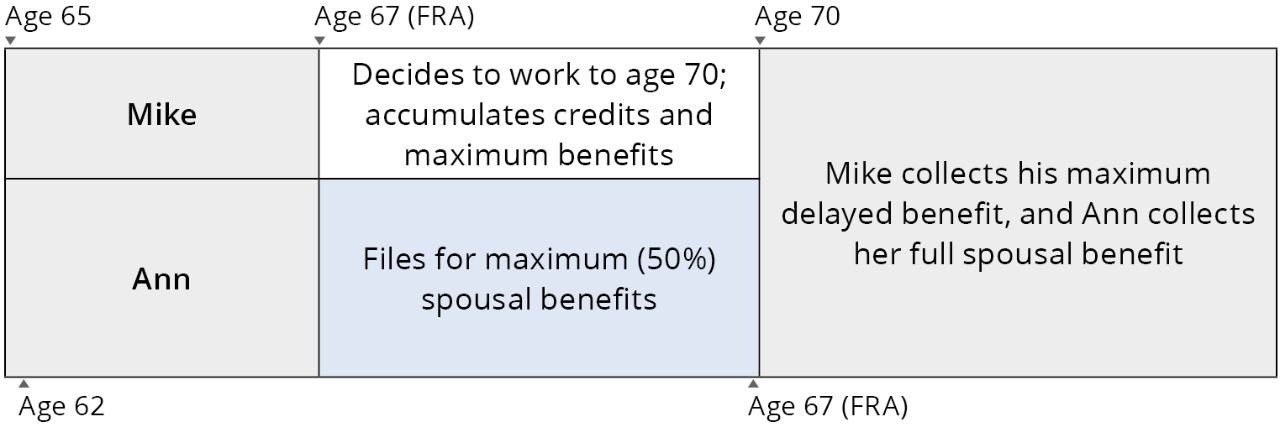

The strategy that works best for you ultimately depends on a host of factors, including: age differences, career earnings, level of savings, health status, and the date of your FRA (FIGURE 1).

We’ll take a close look at three hypothetical couples—Joe and Ruth, Ann and Mike, and Norm and Karen—each approaching the claiming decision from different vantage points. But first, let’s review some of the basic Social Security rules that can impact whether some combination of regular benefits and spousal benefits may be right for you to consider.