Pre-Sales Support

Mutual Funds and ETFs - 800-456-7526

Monday-Thursday: 8:00 a.m. – 6:00 p.m. ET

Friday: 8:00 a.m. – 5:00 p.m. ET

Post-Sales and Website Support

888-843-7824

Monday-Friday: 9:00 a.m. - 6:00 p.m. ET

One of the main advantages of a 529 plan is the ability to grow your education savings tax-free. Those tax benefits also apply once you begin withdrawing from the account as long as the funds are used toward eligible expenses. Because nonqualified withdrawals are taxed as ordinary income and may incur a 10% federal income-tax penalty, the list below can help you avoid unnecessary taxes and make the most of your savings.

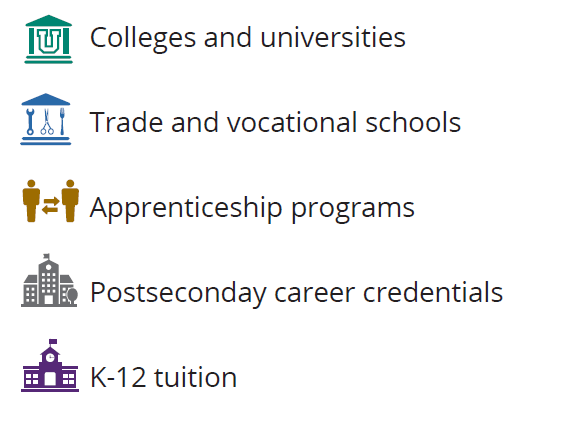

| 1 | College and university tuition – Whether your child attends a public or private university or community college, funds in a 529 account can be used toward tuition as long as the school is eligible for federal student aid. The same is also true for graduate school and some schools abroad. |

| 2 | College alternatives – More Americans have been moving away from more traditional college programs in favor of trade programs, which are often cheaper, offer focused training, and typically take less than two years. 529 accounts can now be used for trade and vocational schools, apprenticeship programs,1 and approved nondegree programs and recognized postsecondary career credentials.2 |

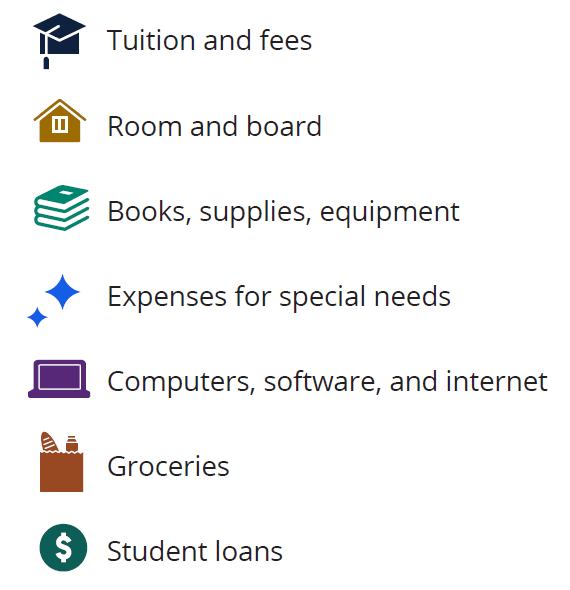

| 3 | Living on or off campus – As long as your child is enrolled in a degree or certificate-seeking program at least half time, room and board on campus is considered a qualified expense. For those living off campus, the cost of rent and utilities up to the school’s allotment is considered qualified, but any amount above the allowance could be subject to taxes. |

| 4 | Groceries – If your child is living off campus, food expenses up to the cost of an on-campus dining plan can be covered by 529 funds, but the tax advantage only applies to necessities—not dining out or entertainment costs. It’s best to confirm acceptable amounts with your child’s school each year. |

| 5 | Academic fees – Students may need to pay fees in addition to tuition, such as technology or lab fees, and can use their 529 plan funds toward them. Activity fees for sports or organizations, however, aren’t eligible. |

| 6 | Computers, software, and internet access – Tech essentials and specialized software required to complete coursework (i.e., any design programs necessary for a graphic-design degree) are considered qualified expenses. Internet access is also a covered expense for students who live off campus. |

| 7 | Books and supplies – In addition to textbooks and class-specific materials, school and office supplies, such as notebooks, pens, pencils, are covered by 529 funds. |

| 8 | K–12 schooling – Up to $20,000 can be used for private or religious K–12 tuition per student, per year. In addition, 529 funds may cover other eligible expenses such as curriculum materials, books, tutoring, standardized test fees, dual-enrollment courses, and certain educational therapies for students with disabilities.2 Check your state’s guidelines to confirm what qualifies. |

| 9 | Student-loan repayment – Funds can be used for qualifying student-loan repayments, which can include both private and federal student loans. When using 529 funds to pay off student debt, there’s a lifetime limit of $10,000. |

| 10 | Roth IRA conversion – Account owners and beneficiaries can now roll over funds into a beneficiary-owned Roth IRA. In order to do so, the 529 account must have been opened for at least 15 years, and the amount rolled over must have been in the account for at least last five years. Rollovers have a lifetime limit of up to $35,000, but they’re also subject to annual IRA contribution limits. |

Qualified Tuition Expenses:

Qualified Education Expenses:

Talk to your financial professional to make the most of a 529 plan.

1 529 plans can be used for apprenticeship programs registered and certified with the Secretary of Labor under the National Apprenticeship Act.

2 To learn more, please refer to the official version of the OBBBA (H.R. 1) at congress.gov.

Sources: Hartford Funds, IRS.gov, and savingforcollege.com, 12/25.

This information has been prepared from sources believed reliable but the accuracy and completeness of the information cannot be guaranteed. This material and/or its contents are current at the time of writing and are subject to change without notice.

This material is provided for educational purposes only. The preceding is not tax or legal advice. Please consult with a tax professional for more information.

State tax treatment may vary from federal tax treatment when using withdrawals from a 529 account for K-12 tuition, apprenticeship costs, or student loan repayment. Consult with a qualified tax or legal professional to learn more.

Before investing, an investor should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s 529 plan.

For more information about any 529 college savings plan, contact the plan provider to obtain a Program Description, which includes investment objectives, risks, charges, expenses, and other information; read and consider it carefully before investing. Hartford Funds Distributors, LLC serves as distributor and underwriter for some 529 plans.