In a situation that would have Sir Isaac Newton rolling in his grave, we’re disproving gravity: what went down (interest rates) must come back up.

Low rates can help spur economic growth by making it cheaper for consumers and businesses to borrow money; conversely, higher rates can be used to cool off an economy that’s too hot. Rates were near zero to support the economy during the COVID-19 pandemic, but with today’s high inflation, the US Federal Reserve (Fed) is increasing rates in an attempt to stabilize prices.

What Do Rates Have to Do With Inflation?

The Fed sets monetary policy to try to keep the economy humming along with full employment and stable prices. One item in its toolbox is the ability to adjust the federal funds rate, or the rate that banks borrow money from each other. This baseline rate influences interest rates on everything from mortgages and car loans to the interest earned on savings accounts or certificates of deposit (CDs).

Today, with a growing economy and rapidly rising prices, the Fed can raise the federal funds rate to discourage spending by both consumers and companies, which should reduce demand and help rein in inflation. But raising rates will have some other ripple effects, too.

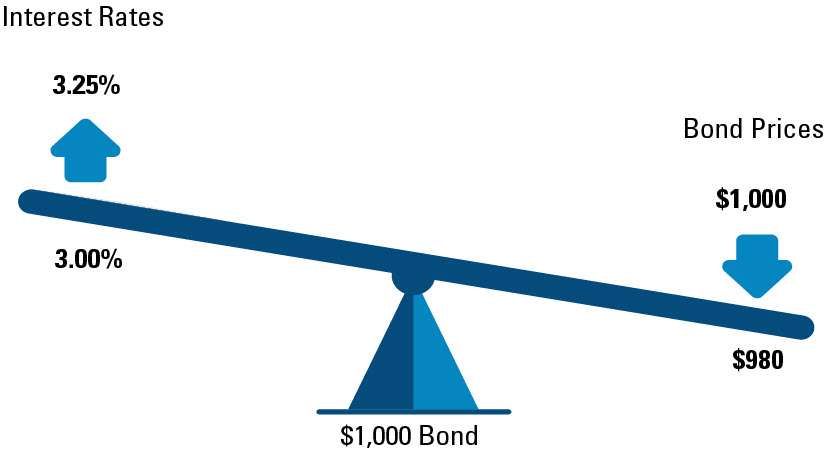

How Might Rising Rates Impact Me?