Pre-Sales Support

Mutual Funds and ETFs - 800-456-7526

Monday-Thursday: 8:00 a.m. – 6:00 p.m. ET

Friday: 8:00 a.m. – 5:00 p.m. ET

Post-Sales and Website Support

888-843-7824

Monday-Friday: 9:00 a.m. - 6:00 p.m. ET

Have you ever had an anxious client declare, “I can’t take it anymore. Pull everything out of the market. We’re going to lose it all!” He watches the media forecasting inevitable losses because of geopolitical concerns in Ukraine/Russia, China/Taiwan, and Iran and North Korea, to name a few. The Fed is raising rates too quickly. Inflation has risen to 40-year highs. Housing and consumer spending are down. And the list of doom and gloom goes on.

When we encounter these kinds of reactions, it’s natural to respond by saying things like, “It’s going to be okay. We’re in this for the long haul.” However, this time-tested approach is out of date and can frustrate a client who is constantly bombarded by a negative news cycle. I use a different approach that may help you too.

First, Relate to Emotions

Even with good intentions, telling a client “It’s going to be okay” can make the client feel like you’re invalidating how they’re feeling. Doing so could make them think you’re minimizing those feelings, implying they shouldn’t be feeling as they do, and dismissing their concerns.

Instead, normalize your client’s feelings. Do this by saying something like, “You’re definitely not alone in how you’re feeling. I have other clients feeling the same way.” It tells the client, “You’re not the only one going through this” and “other people have similar worries.” Normalizing is an effective way to validate your client’s feelings.

I continued: “I don’t know about you, but I am sick and tired of hearing that we’re experiencing ‘unprecedented’ times.” Saying this doesn’t signal that you agree with their recommendation to change their portfolio; it just lets your client know you’ve heard the same news stories and don’t disagree that the Ukraine/Russia conflict, supply-chain issues, or inflation aren’t major issues impacting markets.

Next, I thanked him for sharing his thoughts and told him that he’d done the right thing by coming to me. I could sense that his anxiety level had dropped a bit. Then, I knew I had to address his suggestion to move to cash.

Second, Remember When…

After calming my client’s nerves, the stage was set to reframe the market pullback as an opportunity. I continued: “You know, as much as we’d like things to get back to normal, I doubt they will in the near term.” I elaborated further: “It may take months or years to break even from losses incurred in a bear market.” My client responded, “Exactly, let’s move to cash.” I said, “Before we do that, I have a little historical quiz for you. Can you tell me what the dates of October 9, 2002, March 9, 2009, and March 23, 2020 all have in common?”

In my experience, most clients can’t recall the significance of all three dates so it’s safe to assume you’ll get a blank stare in response.

Point out that they were the market lows from the dot-com crash, the Great Recession, and the COVID-19 pandemic. And that all three were very real and painful downturns that caused a lot of sleepless nights for some people.

Simply asking clients if they remember these dates and how they felt can bring back important memories. If they need some help remembering these events, I suggest saying things such as “I remember back in March of 2009 that some people thought the market was heading to zero.” Or, “Things felt so overwhelming and out of control when COVID hit and the Dow dropped below 20,000, didn’t it? Some people were saying the next leg down would be below 10,000.”

Then, I said: “Let me ask you, if you could go back in time to one of those market lows, what advice would you give yourself and what would you invest your money in?”

You can guess the answer you’ll likely hear: Stocks or equities. Clients say this because they realize that stocks have recovered and moved higher. What you likely won’t hear: Go to cash. Then, I helped him rethink his “all-cash” investment suggestion.

What Do These Dates Have in Common?

Have a conversation with anxious clients about what these dates have in common. (Hint: They’re bear market bottoms).

Source: Ned Davis Research and Hartford Funds, 2024.

Third, What Should We Do Now?

Once I could see that my client’s desire not to miss out on the best part of the next recovery was overtaking his fear of losing more, we were able to have a productive conversation.

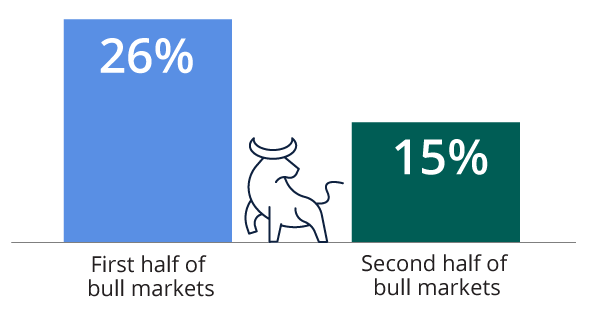

Next, I said: “Sadly, in 2002, 2009, and 2020, I had a few clients who said they couldn’t take it anymore.” I explained how they were adamant to move to cash. I then told him how they missed the first part of the recoveries, then got back in later, after they’d missed the subsequent bull markets’ biggest gains. I shared that for the last ten bull markets, the first halves returned 26% while the second halves returned 15%.

“Why do you think that markets turn positive even during recessions when things seem so bleak?” I asked. My client didn’t know. I continued, “It’s because the market often anticipates better economic conditions when things seem like they’ll keep getting worse.”

I closed our conversation by reconfirming that it’s normal and OK to be concerned about losing more. But by letting those feelings turn into actions, he could be hurting his chances of reaching the goals in the financial plan we built together. We also discussed how staying invested would enable him to take part in the momentum of a recovery from day one.

Don’t Miss the First Half

The last 10 bull markets—First halves outperformed

Past performance does not guarantee future results. Investors cannot invest directly in indices.

The S&P 500 Index is used to represent the last ten bull markets. The S&P 500 Index is a composite of 500 leading companies in the United States.

Source: Morningstar and Hartford Funds, 2024.

What if a Client Still Wants to Go to Cash?

Sometimes, after I’ve empathized with a client’s anxious feelings, discussed previous bottoms and recoveries, and explained the potential consequences of going to cash, I’ve still had clients insist on going to cash. At that point, it can make sense to consider some de-risking ideas, such as dividend-paying stocks, US Government bonds, or moving a portion to cash instead of everything.

To Summarize

First, help clients realize that being concerned about further losses and thinking the bottom hasn’t occurred yet is perfectly normal. Second, help them remember past bear-market bottoms and recoveries. Third, explain the potential consequences of going to cash and missing the first part of recoveries.

My Client Backed Off the Ledge

In most cases, clients leave my office feeling better and less worried about the near-term performance of their portfolio and the markets. Most of them express gratitude for taking the time to help them avoid a potential investment mistake. As the conversation wraps up, I always thank them for not only trusting me with their life savings, but also with their fears, thoughts, and concerns. I let them know it’s helpful for me to know what they are thinking and feeling because if they are going down that path, other clients are too.

Next Step

The next time an anxious client suggests moving to cash because of market volatility, acknowledge and empathize with their feelings. Then, ask them what October 9, 2002, March 9, 2009, and March 23, 2020 have in common.

Robert Laura is a pioneer in the psychology and social science of retirement planning. He’s a three-time best-selling author, nationally syndicated columnist for Forbes and Financial Advisor Magazine and recognized presenter at retirement conferences across the country. As a former social worker turned money manager, author, and speaker, his work has reached millions of people through seven books, twelve guides, and over 800 articles. He frequently appears in major business media outlets such as the Wall Street Journal, USA Today, CNBC, MarketWatch, The New York Times, and more.

Investing involves risk, including the possible loss of principal. For dividend-paying stocks, dividends are not guaranteed and may decrease without notice.

The views and opinions expressed herein are those of the author, who is not affiliated with Hartford Funds.