Pre-Sales Support

Mutual Funds and ETFs - 800-456-7526

Monday-Thursday: 8:00 a.m. – 6:00 p.m. ET

Friday: 8:00 a.m. – 5:00 p.m. ET

Post-Sales and Website Support

888-843-7824

Monday-Friday: 9:00 a.m. - 6:00 p.m. ET

At 75, Diane was a widow collecting a modest Social Security retirement benefit of just over $1,000 a month. After attending a Social Security workshop, Diane was stunned to learn she had been eligible for a survivor benefit of $2,400 per month based on her late husband’s earnings. That’s $1,400 more every single month—money she desperately needed and rightfully deserved.

Over five years, Diane missed out on more than $84,000.

Her story is a powerful reminder: not knowing their options can cost a surviving spouse dearly. Widows and widowers owe it to themselves to explore both retirement and survivor benefits, because understanding these options can make a significant difference in their financial well-being.

First, What Surviving Spouses Are Entitled to1

The Survivor Benefit

If the higher-earning spouse dies, the surviving spouse is typically entitled to the greater of their own benefit or up to 100% of the deceased spouse’s benefit. In other words, if the deceased spouse had a higher benefit, the survivor could switch to that higher amount.

Let’s use Kent and Amy as an example. Stepping out of the workforce to care for aging parents resulted in a lower individual retirement benefit for Amy. When Kent passed away, she became eligible for Kent’s benefit, increasing the amount she received by more than 50%.

Individual vs. Survivor Benefits

| Kent $4,000 |

|

If Kent passes away, Amy may be entitled to 100% of Marc’s benefit  |

| Amy $1,900 |

|

General eligibility guidelines:

A couple must have been married for at least nine months (and the surviving spouse must not remarry before age 60)

The surviving spouse must be at least age 60; however, filing before their full retirement age (FRA) is considered early and may reduce the benefit amount

A spouse is entitled to the greater of their own benefit or the survivor benefit—but not both

If a lower‑earning spouse is already receiving a spousal benefit when the higher‑earning spouse passes away, Social Security will, in most cases, automatically convert it to a survivor benefit once the death is reported. The surviving spouse may still need to contact the Social Security Administration for the one‑time $255 death payment, but not for the monthly survivor-benefit conversion.

Unfortunately for Diane, she didn’t realize this, leading to a significant financial loss at an already difficult time. That’s why understanding your options is so important—but it’s only the first step. The next is knowing how to claim them in a way that supports your long-term goals.

Second, Claiming Strategies for Surviving Spouses

If the surviving spouse hasn’t yet applied for either a spousal or individual benefit, they may have valuable filing options to consider—based on their unique needs and preferences.

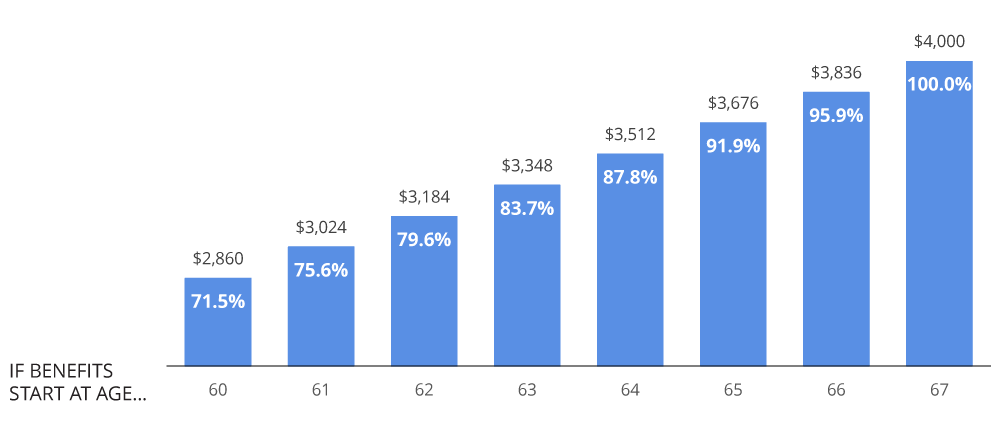

Today’s FRA is 67,2 and at that age, your Social Security benefit is paid at its full amount, without any reduction for early filing. As the bar chart below shows, claiming benefits earlier (such as at age 62) results in a permanently lower monthly payment, because those benefits are expected to be paid over a longer period of time. By contrast, waiting until FRA means fewer years of payments but at a higher monthly amount.

Early Claiming Strategy

A surviving spouse can claim survivor benefits as early as age 60 (or 50 if disabled), but filing before FRA permanently reduces the benefit. The earlier they file, the larger the reduction. For example, claiming at age 60 provides only about 71.5% of the full benefit, while claiming at 61 provides about 75.6%, and so on. (See Figure 1.)

Maximizing Strategy

By waiting until FRA, the surviving spouse can receive 100% of the deceased spouse’s benefit, offering a higher level of support over time.

Figure 1: Early vs. Delayed Filing: How It Affects Survivor Benefits

Portion that would be received assuming survivor benefit of $4,000 at a Full Retirement Age (FRA) of 67*

Note: Survivor benefits have their own FRA schedule, which is slightly different from the individual FRA. Benefits are subject to the earnings test and will be reduced if the survivor is still working and receiving earned income.

*What you could get from survivor benefits, ssa.gov, 2/26.

Switch Strategy

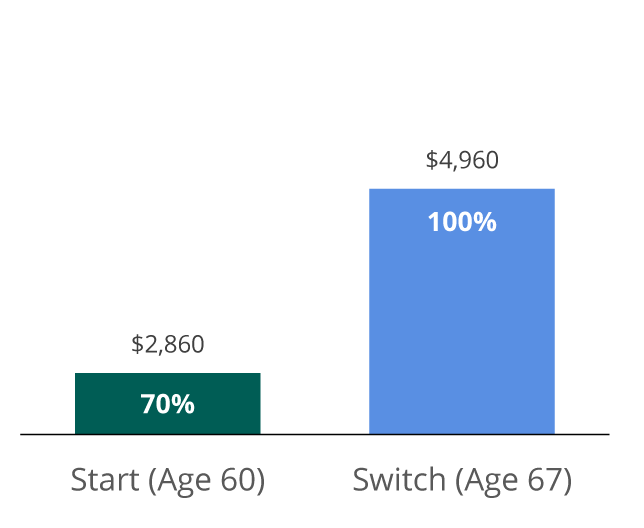

Suppose Kent passed away before Amy reached her FRA, and she was only 62. Since she’s eligible, she may choose to file for her own smaller benefit. Filing early for her individual benefit would reduce that amount, but it would still provide her with some income. It would also allow the survivor benefit to remain untouched until she reaches her FRA of 67. At that point, she could switch to the survivor benefit and receive 100% of Kent’s benefit as his surviving spouse. Survivor benefits do not increase beyond FRA, so waiting past age 67 would not result in a higher survivor benefit. (See Figure 2.)

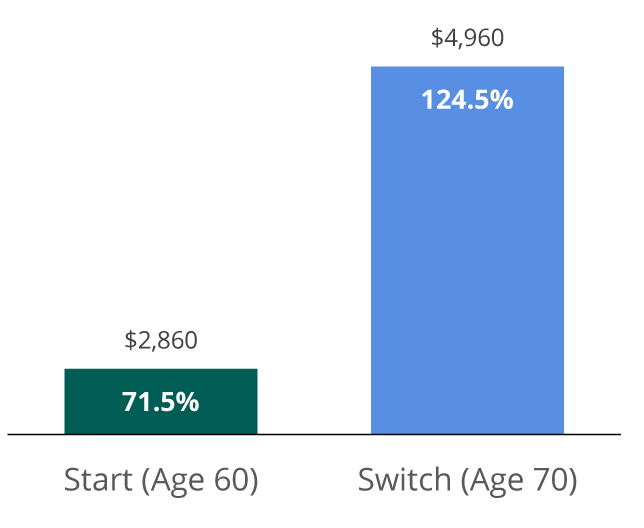

Conversely, if Amy passed away first, Kent might choose to claim the lower survivor benefit initially. This approach would allow his own retirement benefit to continue growing, since it would earn delayed retirement credits until he reaches age 70. At that point, he could switch to his higher individual retirement benefit. Unlike survivor benefits, an individual’s own retirement benefit can continue increasing until age 70. (See Figure 2.)

In both cases, the advantage is the same: by starting with the smaller benefit, the surviving spouse preserves the higher benefit for later, ultimately increasing their income over time. Now that we’ve seen how this works for married spouses, we can turn to how similar strategies apply—though with different rules—to divorced surviving spouses.

Figure 2: Switch Strategy

Switch Strategy 1:

Amy Claims Her Own Benefit First,

Then Switches to Survivor Benefit

Switch Strategy 2:

Kent Claims Survivor Benefit First,

Then Switches to His Own

Third, Survivor Benefits for Divorced Surviving Spouses

If eligibility requirements are met, a divorced surviving spouse can use the same Social Security claiming strategies as a married surviving spouse—i.e., Early, Maximizing, and Switch—but the guidelines differ.

General eligibility guidelines:

The marriage must have lasted for at least 10 years

The surviving divorced spouse must be at least age 60 (or age 50 if disabled).

Remarrying before age 60 generally makes a surviving divorced spouse ineligible for survivor benefits on a former spouse’s record. Remarriage after age 60 preserves eligibility.

How to apply for survivor benefits

Again, unlike many other Social Security benefits, there is currently no online application process for survivor benefits. To apply, you must either call the SSA or contact your local Social Security office to complete the application by phone or in person.

You’ll need the following documents on hand:

Proof of death (often reported by a funeral home)

Your birth certificate or other identification Your marriage certificate (or divorce decree*)

Social Security numbers for both you and the deceased

If a divorced spouse can’t obtain their ex-spouse’s death certificate when applying for survivor benefits, the SSA may still be able to help. Often, the death is already reported to SSA by the funeral home. Otherwise, the applicant may need to provide identifying details (such as the ex-spouse’s name, SSN, and date of birth), along with a marriage certificate and divorce decree. If needed, SSA can assist in verifying the death through other records.

To Summarize

First, a surviving spouse is generally entitled to receive the higher of their own benefit or up to 100% of the deceased spouse’s benefit. Second, if a surviving spouse hasn’t yet filed for spousal or individual benefits, they may have valuable claiming strategies available to them. Third, if eligibility criteria are met, a divorced surviving spouse can use the same Social Security claiming strategies as a married surviving spouse.

Navigating Social Security after the loss of a spouse can feel especially overwhelming.

Gaining a clear understanding of available options can provide a sense of direction during a time when so much feels uncertain. Whether married or divorced, filing early or coordinating benefits for future maximization, surviving spouses have important choices that deserve thoughtful consideration.

Diane’s story is a reminder of what may be at stake. The goal isn’t simply to avoid missing out—it’s to make the decision that best supports your financial future.

Curtis is a senior internal advisor consultant for Hartford Funds. He supports financial professionals and their clients with educational materials, product expertise, and practice-management strategies.

1 Benefits for Spouses, ssa.gov, 2025

2 Retirement Planner: Full Retirement Age, ssa.gov, 2025

All information provided is for informational and educational purposes only and is not intended to provide investment, tax, accounting or legal advice. As with all matters of an investment, tax, or legal nature, you should consult with a qualified tax or legal professional regarding your specific legal or tax situation, as applicable.