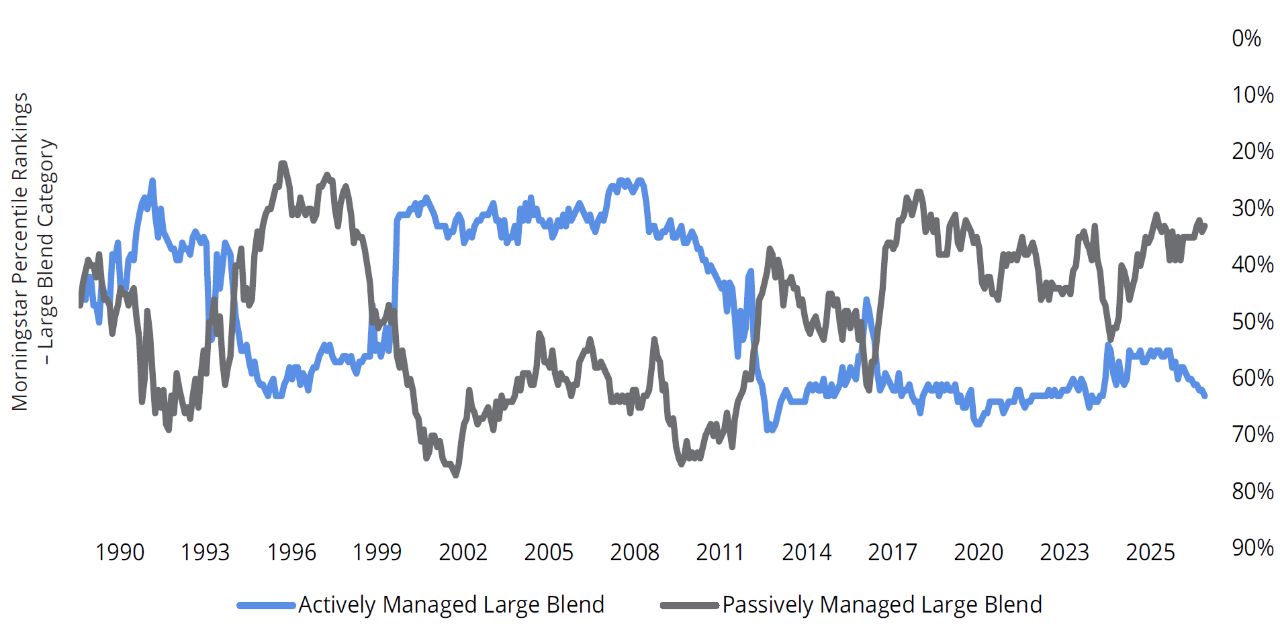

Active Management Has Fared Better During Corrections

When corrections occur, you may not want to be exclusively invested in passive. Instead, you may want to consider investing in actively managed funds.

There have been 27 market corrections over the last 35 years. FIGURE 6 shows that during those corrections, active outperformed passive 21 times, with an average rate of outperformance of 1.05%. Again, we compared active to passive by removing index and enhanced index funds from the Morningstar Large Blend Category to represent active, and used the S&P 500 Tracking Index category to represent passive.

By allowing investors to respond to ever-changing markets, active management empowers investors to maximize opportunity as conditions demand. But if you’re invested in an index fund, you could be exposed to significant downside due to single-sector performance. For example, during the collapse of the dot-com bubble in 2000, active management outperformed passive significantly, -2.41% to -9.42%.3 Much of the blame for passive’s underperformance during that period can be laid at the feet of a single sector.

As FIGURE 7 shows, the technology sector made up 28% of the S&P 500 Index at that time. The sector (as represented by the S&P 500 Information Technology Index) crashed hard, to the tune of a 38.72% decline in 2000.

Meanwhile, the average active manager was underweight technology relative to the index (23% vs. 28%), which helped limit the damage done to their portfolios when the tech bubble burst. Active managers with a positive return during this time were more underweight to technology with a 12.3% average weighting, and those with a negative return hewed closer to the index with a 32.8% average weighting.4

When bull markets inevitably turn, passive managers could be left holding stocks and sectors with poor fundamentals and inflated valuations. Meanwhile, active managers have the ability to help mitigate risk by reducing exposures to expensive areas that will be hit hardest, and conversely, increase exposure as sectors or asset classes recover to capture upside as the new market cycle begins.