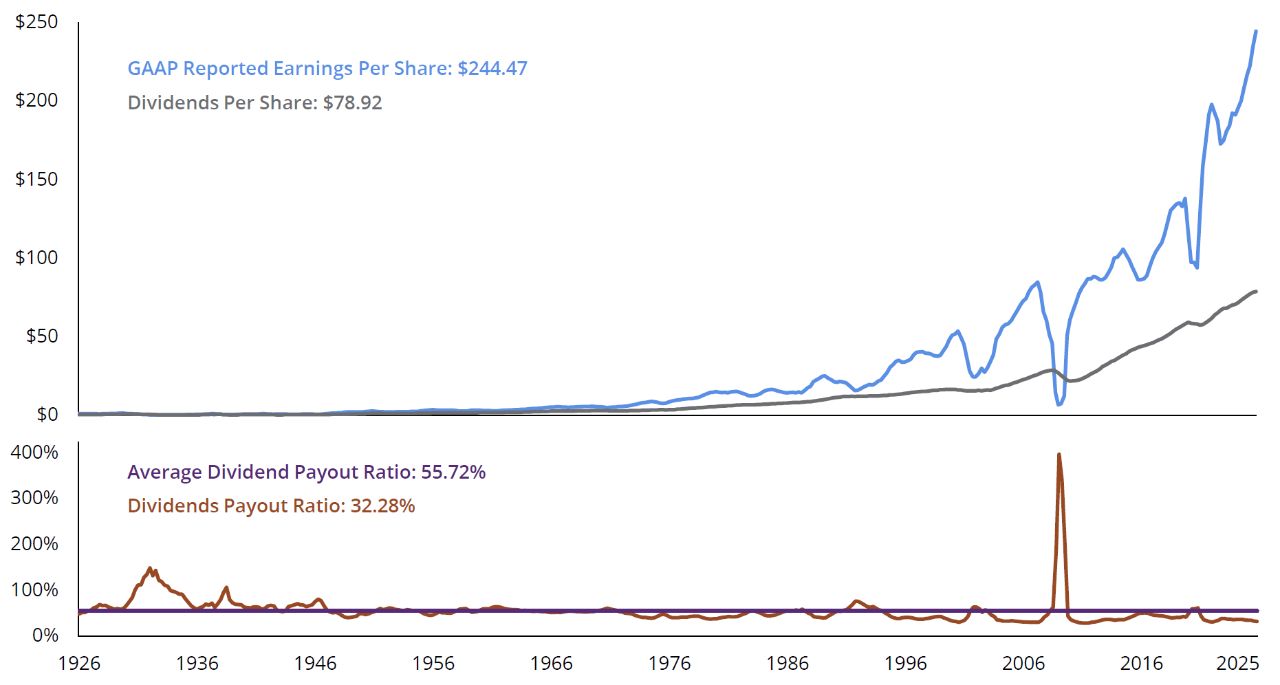

Trend 2: Many Retirees Are Seeking Yield and Capital Appreciation

Although bond yields have risen and can offer predictable income, bonds haven’t historically offered as much capital appreciation as stocks. Dividend-paying stocks may be appealing to many investors who are seeking yield along with growth potential. For example, retiring baby boomers who are searching for income-producing investments and institutional investors seeking yield may find dividend-paying stocks to be an attractive option.

Trend 3: Financial Repression and Institutional Investors

Following a prolonged period of near‑zero rates after the GFC, the US Federal Reserve (Fed) aggressively raised interest rates to combat post‑pandemic inflation. While rate cuts began in late 2024, the pace of easing slowed considerably through 2025. In 2026, interest rates remain elevated relative to the prior decade, reflecting a policy environment shaped by more than just short‑term economic cycles.

We generally think of monetary policy as a catalyst to help accelerate or decelerate economic activity, but it can also serve other purposes. During the prolonged low-rate era following the GFC, low interest rates benefited not only businesses and consumers who wanted to borrow money, but also the biggest debtor in the world, the US government, by keeping interest payments on the national debt manageable.

Now that rates have risen, that dynamic has shifted. Savers who were receiving startlingly low rates on CDs,9 money-market funds,10 and savings accounts11 are now earning more attractive yields. But higher rates have also increased the cost of servicing the national debt, putting additional pressure on an already burgeoning level of US government borrowing.

Low interest rates are especially problematic for institutional investors. How long can a pension plan with an actuarial discount rate of 6% or higher continue to accept 10-Year US Treasury bonds12 that yield around 4%?

Institutional investors who seek higher interest rates have numerous options, including high-yield bonds,13 bank loans,14 sovereign debt of foreign countries,15 REITs,16 and dividend-paying stocks.17

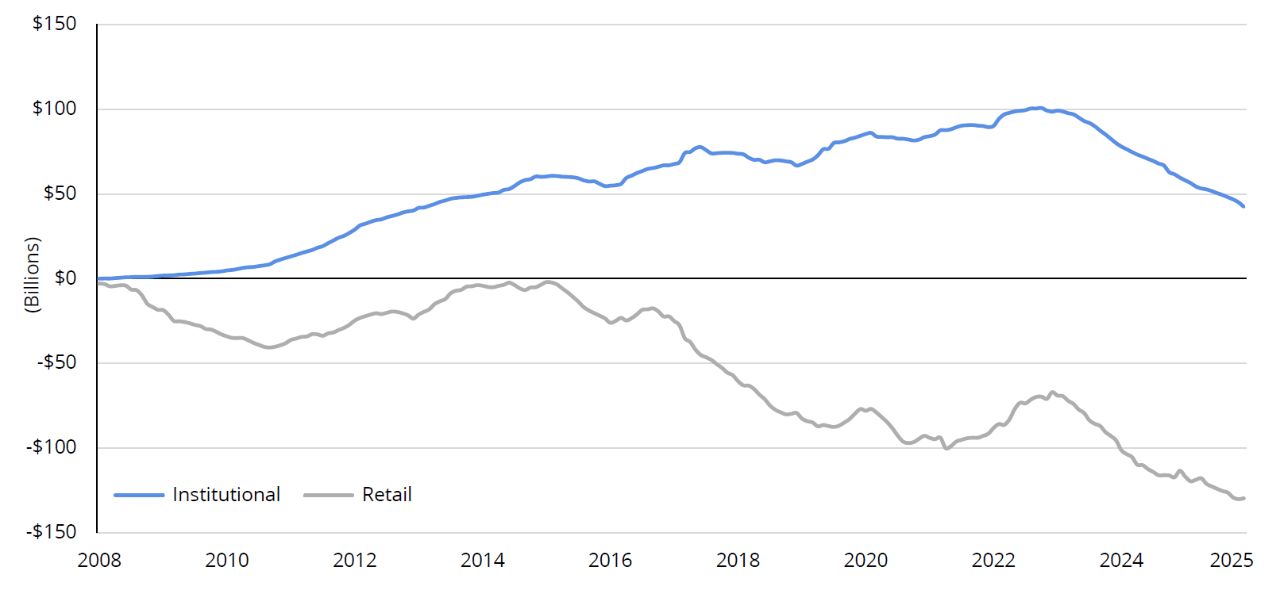

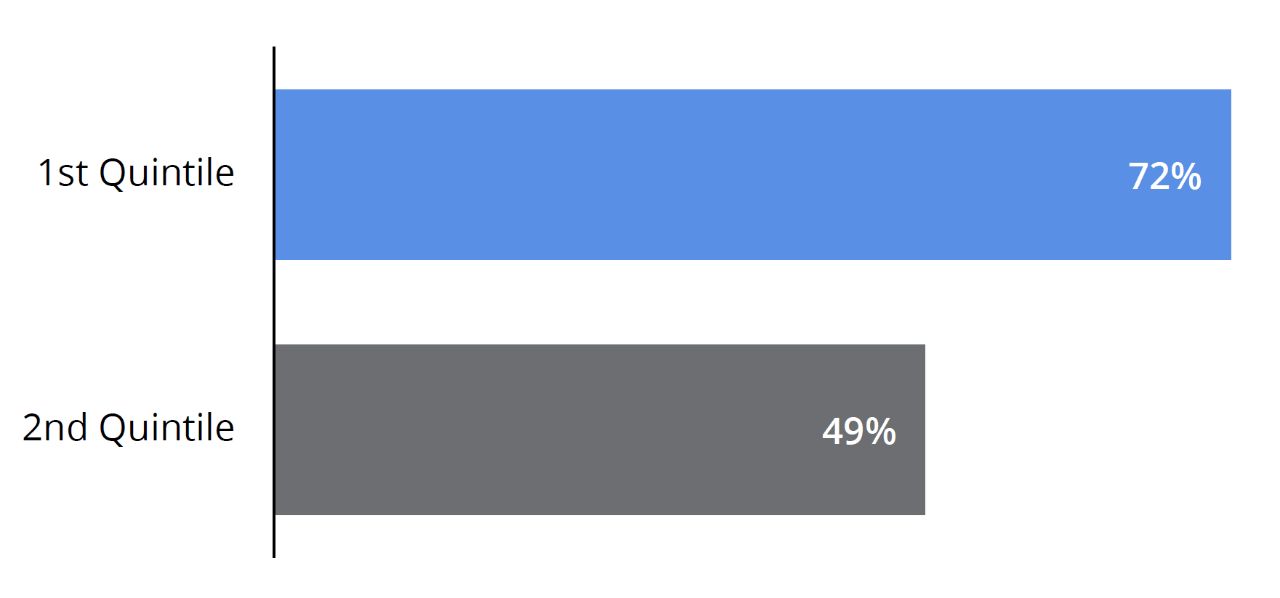

In fact, since 2008, some institutional investors have poured more than $42 billion into equity-income funds while individual investors have withdrawn nearly $130 billion over the same time period (see FIGURE 11). It’s not uncommon for institutional investors to be ahead of the general public when it comes to investing, but how long will this striking disparity last?

More recently, periods of market concentration and heightened volatility have brought renewed attention to dividend‑paying stocks, as both institutional and retail investors reassess sources of return beyond growth‑oriented segments of the market.