Inheriting an IRA can feel overwhelming. Along with the emotional weight that often comes with a loved one’s passing, you’re suddenly faced with important financial decisions—many of them time sensitive—that can have lasting tax consequences.

The rules governing inherited IRAs have changed in recent years, and while the details can be complex, the core question is simple: What are your distribution options, and how do those choices affect your taxes and long-term financial picture?

The answer depends largely on who you are in relation to the original account owner. Under current law, IRA beneficiaries generally fall into one of three categories, each with its own set of rules and opportunities. Let’s look at how these beneficiary types work—and what they may mean for you.

1. Eligible Designated Beneficiaries: Flexible Options

Some beneficiaries are granted more flexibility under the law. Known as eligible designated beneficiaries, this group includes spouses, minor children of the account owner, individuals who are disabled or chronically ill, and beneficiaries who are not more than 10 years younger than the original owner. Spouses also have the option of rolling funds into their own IRAs.

Example:

Tom, 68, who was never married, names his younger brother Steve—just six years his junior—as the beneficiary of his IRA. When Tom passes away, Steve qualifies as an eligible designated beneficiary. Steve has several options:

- Option A: He can withdraw the entire IRA immediately, recognizing the full amount as taxable income in the year of distribution.

- Option B: He can take withdrawals over time, choosing when and how much to distribute, with each withdrawal taxed in the year it’s taken. He can make no contributions to the account, but any assets that remain can continue to potentially grow tax deferred. The account must be depleted within 10 years.

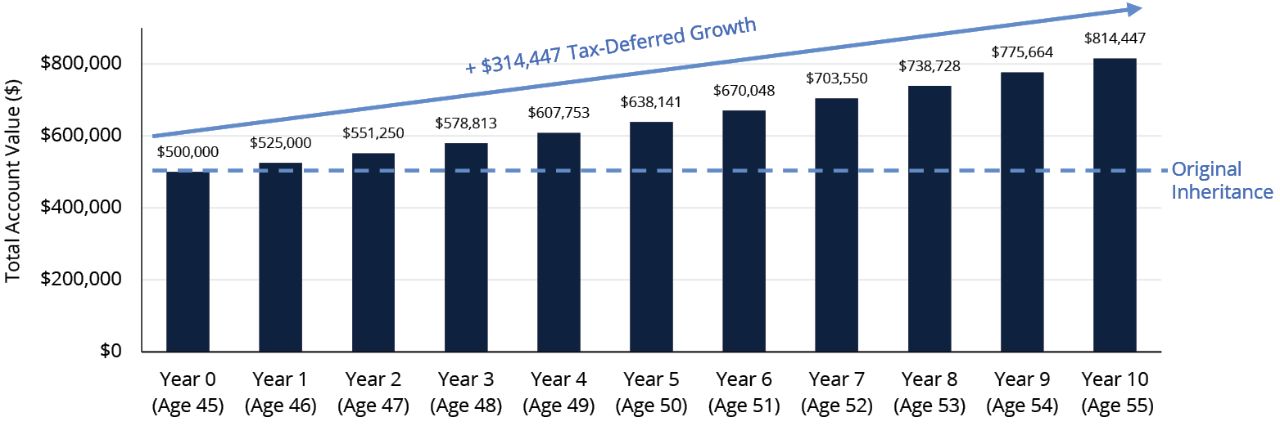

- Option C: He can spread distributions—and mandatory required minimum distribution (RMD) withdrawals—over his own life expectancy, allowing the remaining assets to stay invested and potentially grow tax-deferred.

This last option is often appealing for beneficiaries who don’t need the money right away. It provides access when needed, while helping manage taxes and preserve long-term growth potential. If a beneficiary only withdrew the required minimum each year, the remainder could continue to grow tax-deferred.