Pre-Sales Support

Mutual Funds and ETFs - 800-456-7526

Monday-Thursday: 8:00 a.m. – 6:00 p.m. ET

Friday: 8:00 a.m. – 5:00 p.m. ET

Post-Sales and Website Support

888-843-7824

Monday-Friday: 9:00 a.m. - 6:00 p.m. ET

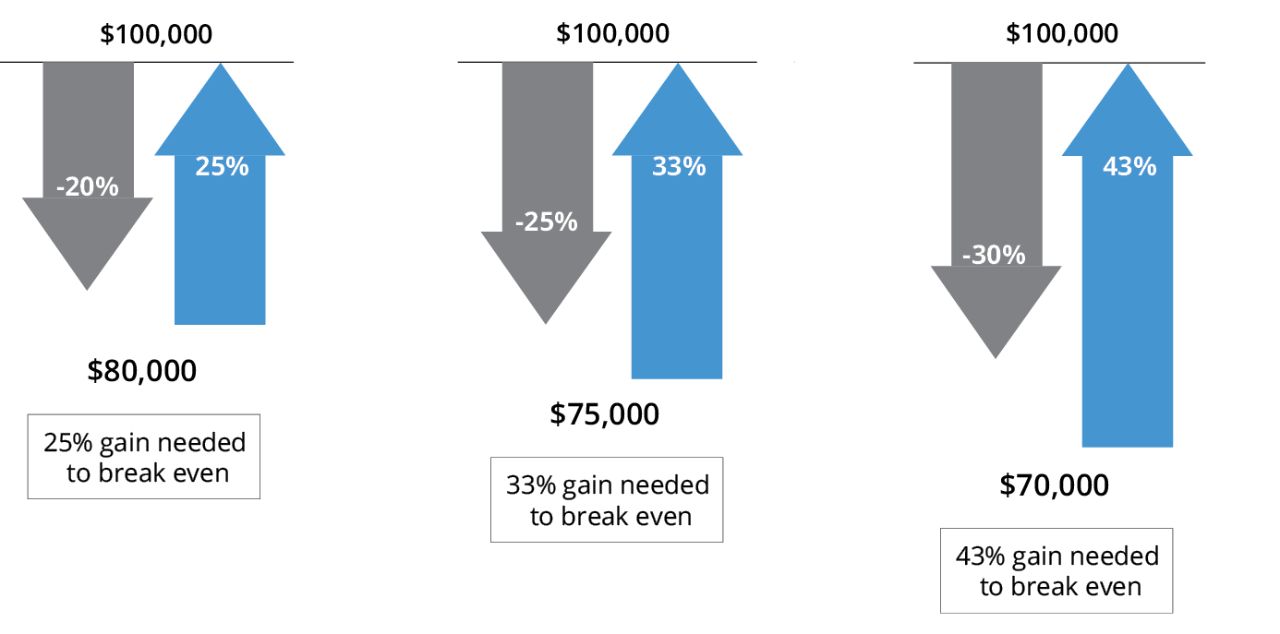

If you’ve been building your nest egg for a while, you’ve seen markets go up and down. But if you’re close to retirement—or already there—a significant loss can be quite painful. That’s because simple arithmetic makes any investment loss tougher to recover from. In percentage terms, the more you lose, the harder it becomes to break even. Therefore, as you near retirement, protecting against losses should be one of your main priorities.

Investment Losses Are Tough, But Breaking Even Can Be Tougher

Below are the gains you’d need to make up for three different loss amounts on a $100,000 initial investment.

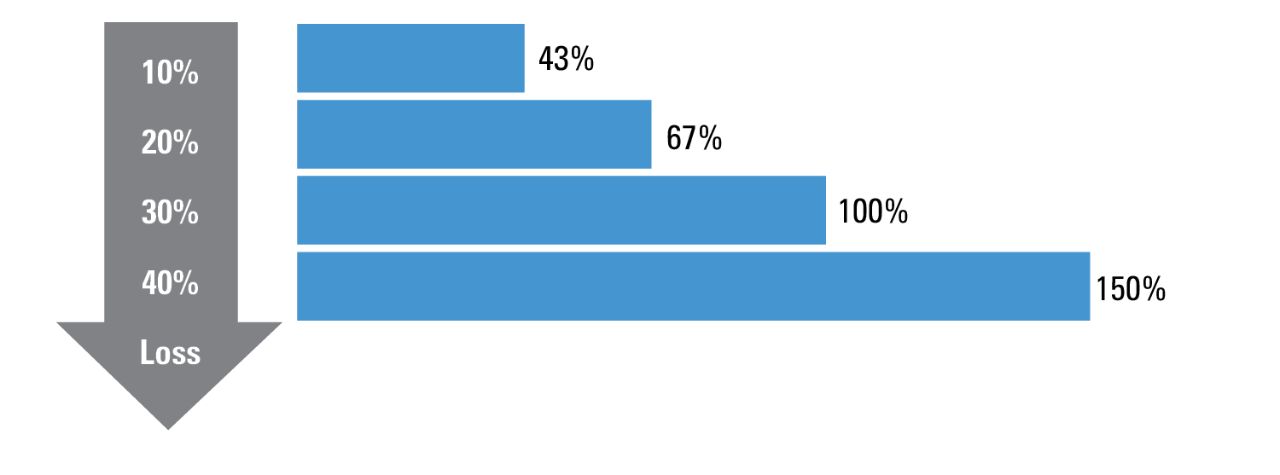

Recouping a loss becomes even tougher if you’re taking annual distributions and no longer adding to your principal.

Cumulative Gain Required to Return to Break Even When Taking 4% Annual Withdrawals

Past performance does not guarantee future results. Investing involves risk, including the possible loss of principal.

The charts above are for illustrative purposes only. The catch-up percentage gains shown in the second chart assume a hypothetical investor opts to take a consistent $4,000 annual distribution for five consecutive years, based on a $100,000 retirement nest egg. The percentages in the downward-facing gray arrow each represent a one-time investment loss over the five-year period of distributions. Source: Hartford Funds

Whether you're nearing retirement or already in it, your financial professional can help you manage risk prudently.

This material is provided for educational purposes only.