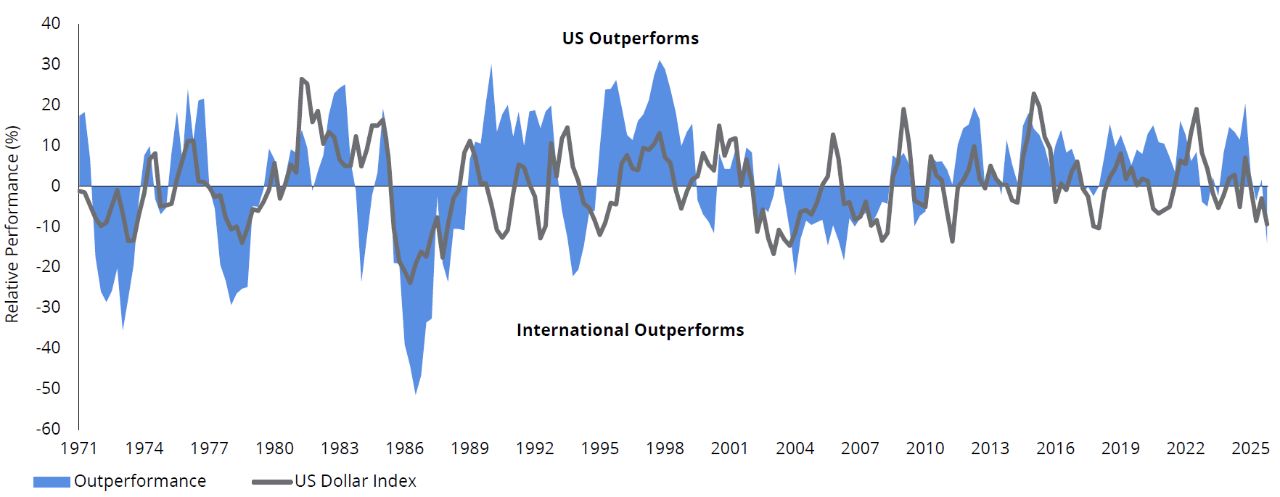

If it ain’t broke, don’t fix it, right? Since US stocks were crushing it for more than a decade, it seemed pointless to look anywhere else for return. But some of the advantages for US stocks may have shifted course, making now a good time to consider a more diversified approach going forward.

For years, interest rates and inflation were low, which favored growth stocks. Strong demand for smarter devices and online services also helped drive impressive outperformance for the tech-heavy US stock market—and for much longer than usual (FIGURE 1).

Then inflation hit multi-decade highs, and the Federal Reserve (Fed) raised US interest rates aggressively in response. This was a challenge for markets, but it may have also hit the reset button. For the first time in many years, value stocks repeatedly outperformed growth stocks abroad.

Can this reset last? We think it could. For starters, inflation can be difficult to truly tame. While it has slowed significantly from its peak, price pressures remain above the Fed’s target, and higher oil prices from the conflict in Iran may also prove inflationary. As a result, policymakers appear inclined to keep rates at relatively restrictive levels until they feel more confident that inflation is firmly under control.