No one likes having their investments lose value or paying more in taxes than they have to. But investment losses can actually be an unlikely hero—one that helps lower your tax bill. Through a strategy known as tax-loss harvesting, once you realize a loss by selling an investment, you can use the loss to reduce your overall taxable income or use it to help offset investment gains on which you’d owe capital-gains taxes.

Got Losses?

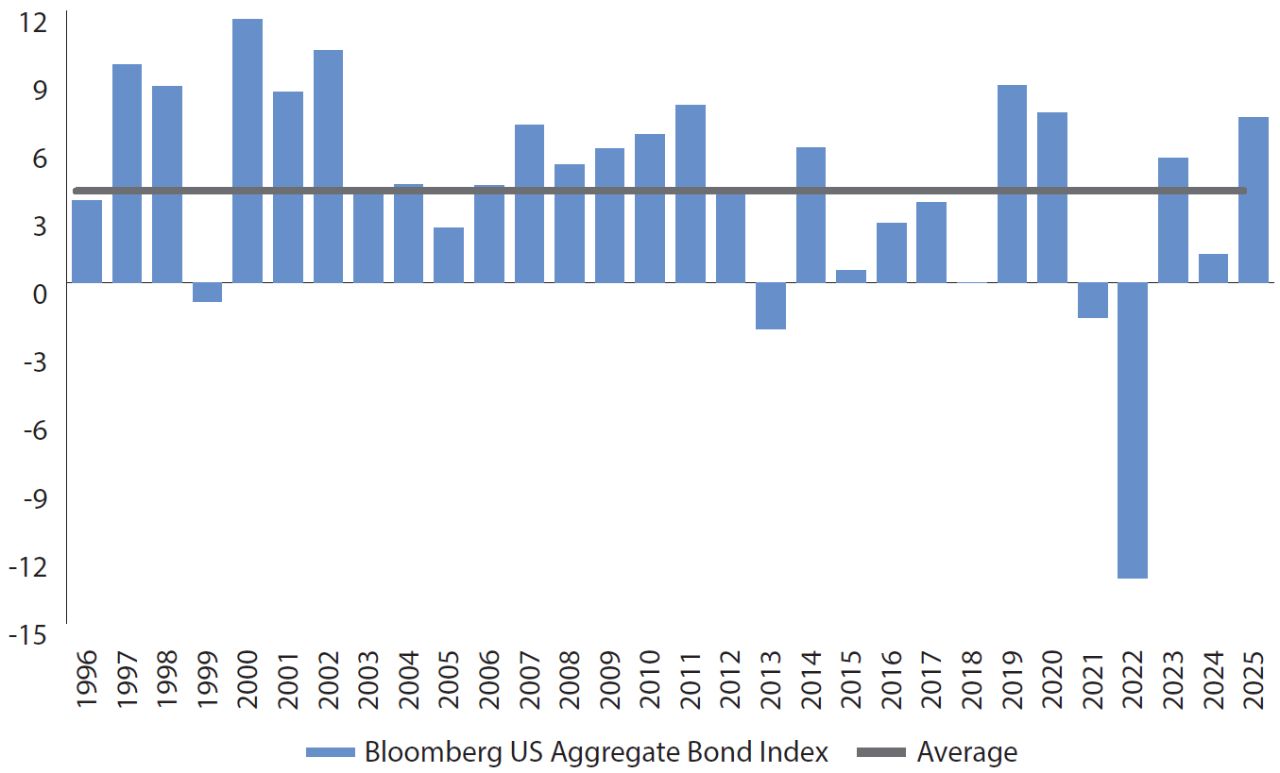

When bonds were negatively impacted by changing interest rates a few years ago, fixed-income investors may have experienced some underwhelming performance. But those losses could still be carried forward to take advantage of tax-loss harvesting and lower your tax liability today.

And despite some recent volatility, there’s still value in being a bond investor. For starters, bonds remain attractively priced by historical standards, even though yields are off their recent highs. In addition, bonds have a self-healing mechanism: If held to maturity (and if they don’t default), they’ll eventually recoup their losses over time. Bonds currently offer attractive yields as well as opportunities for capital appreciation in the future.

This leads to additional advantages of applying tax-loss harvesting: You have the opportunity to rebalance (and potentially upgrade your investments) in a tax-efficient manner.