It’s easy to spot the difference between apples and oranges at your local market. For investors attempting to discern the advantages of tax-free municipal bonds over taxable corporate bonds, it’s more akin to choosing between Fujis and honeycrisps. It takes more than a simple eye test to ensure a fair and accurate comparison.

After all, municipal bonds (“munis” for short) and investment-grade corporate bonds share many common attributes. Both fixed-income types can offer attractive yields, boast relatively high credit quality, and can help diversify equity-heavy portfolios. But since the income earned on munis is generally exempt from federal income taxes, a careful investor needs a reliable tool for sizing up the tax advantages of munis, especially when, at first glance, it might appear that taxable bond yields are superior.

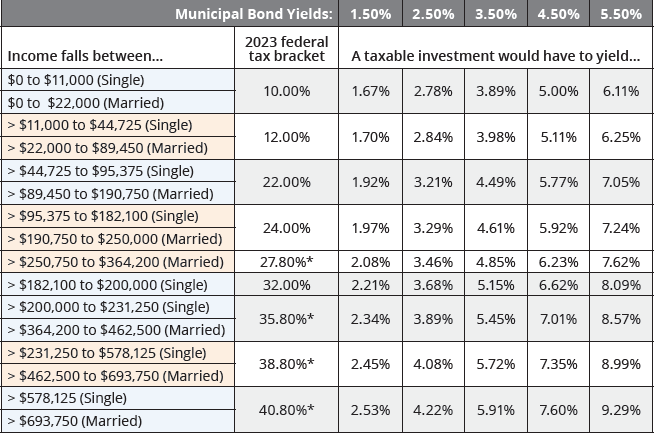

That’s why learning how a municipal bond’s tax-equivalent yield is calculated could be a useful thing to know.

A tax-equivalent yield is the return calculation that puts a taxable bond and tax-exempt muni on equal footing. Computing the tax-equivalent yield helps investors understand how much a tax-exempt bond may save them in taxes. This provides a fairer way to compare the potential tax-free benefits a muni investor could receive vs. taxable alternatives whose yields are quoted pre-tax.

Calculating Your Tax-Equivalent Yield Is Easy

By identifying your current tax bracket, you can quickly calculate whether a municipal bond offers a yield that's competitive with its taxable equivalent. The formula looks like this: