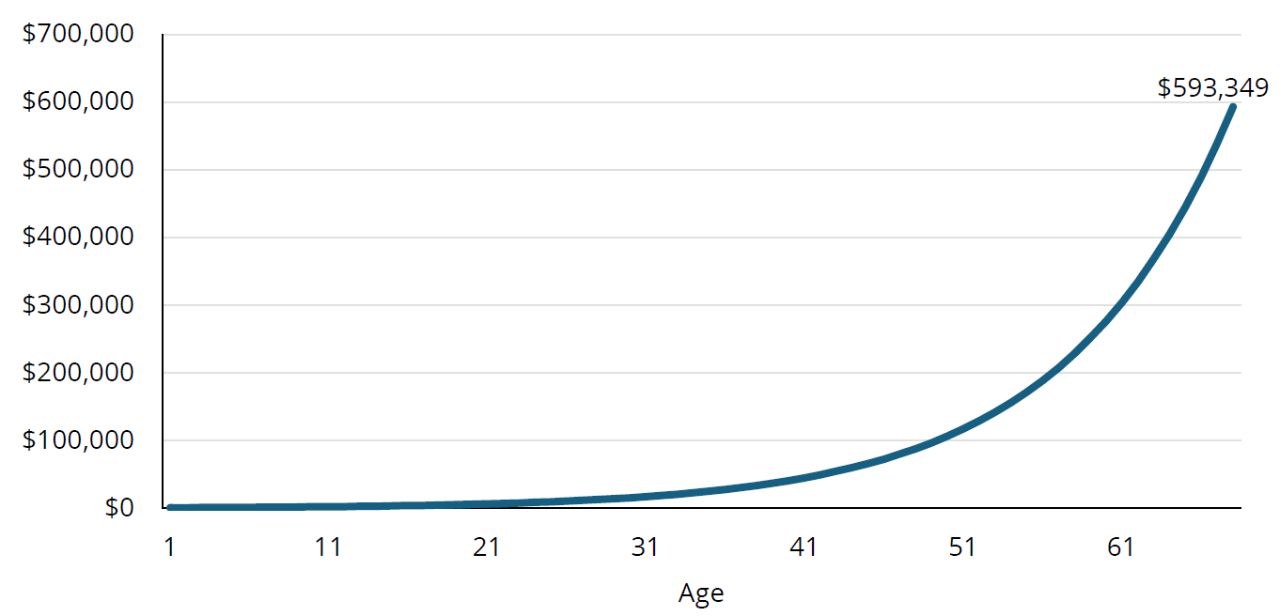

When it comes to building long-term wealth, starting early is one of the most powerful moves a family can make. A child born today has decades before traditional retirement age, which means decades of potential compounding and growth, even with modest contributions.

If you have children under 18, there are two main account types to consider to give your child an early start on their retirement savings: Trump Accounts, which are new and only available as of 2026, and custodial IRAs.

Both are designed to give children an early start on retirement savings via long-term growth. Understanding the similarities and differences between the two types of accounts can help you choose the right fit for your family.

What They Have in Common

Trump accounts and custodial IRAs share some common traits:

- You’re in charge—for now. As a parent or guardian, you manage the account on your child’s behalf until they reach adulthood. For Trump Accounts, control transfers at age 18 under federal law. For custodial IRAs, it depends on your state’s age of majority, which is either 18 or 21.

- The earlier, the better. Both accounts are structured to give your child the full benefit of long-term, tax-advantaged growth, and the earlier you start, the more time compounding has to work.

- Both can be a group effort. Parents, grandparents, and other family members can help contribute to either account, up to certain limits.

As much as they have in common, the differences between the account types could be what makes or breaks your decision. The side-by-side view below can help you compare the key differences between the types of accounts.