Parents Can Help

Parents play a pivotal role in shaping their teen’s financial future—not just by contributing funds, but by modeling smart financial behavior and fostering a mindset of long-term planning. Offering matching or gifted contributions can help teens stay motivated and work toward specific savings milestones. These early contributions, paired with encouragement, can help teens feel that their financial goals are both real and reachable.

While parents are allowed to contribute to a teen’s Roth IRA, it’s crucial to note that the amount parents contribute is still subject to the child’s earned income that they declare to the IRS. IRS rules don’t specify where contributions come from as long as they don’t exceed the child’s earned income for the year.

Beyond dollars, parents can use this opportunity to teach essential financial concepts such as budgeting, compound interest, and the importance of delayed gratification. Discussing investment choices together, reviewing account statements, and setting shared milestones can turn saving into a collaborative learning experience.

Benefits of a Roth IRA

One of the main advantages of a Roth IRA is the ability to withdraw funds tax-free in retirement. For young investors, who are likely in a very low or zero tax bracket, this means investing for retirement now can have a beneficial tax impact later.

Contributions to a Roth IRA can be withdrawn at any time tax-free and penalty-free, though the earnings on those contributions may be subject to a 10% penalty and subject of income taxes under most circumstances. For a withdrawal to be completely tax-free, the account must have been open for at least five years, and the account holder must meet one of the following conditions: reaching age 59½ or older, becoming disabled, using the funds for a first-time home purchase (up to a $10,000 lifetime limit), or the withdrawal being made by a beneficiary after the account holder’s death.

Instilling Good Financial Habits

Early and consistent investing in a Roth IRA helps encourage good saving habits in young people while also growing their retirement funds. Starting during teenage years provides ample time to develop these crucial habits and can help put young investors on a path to financial independence.

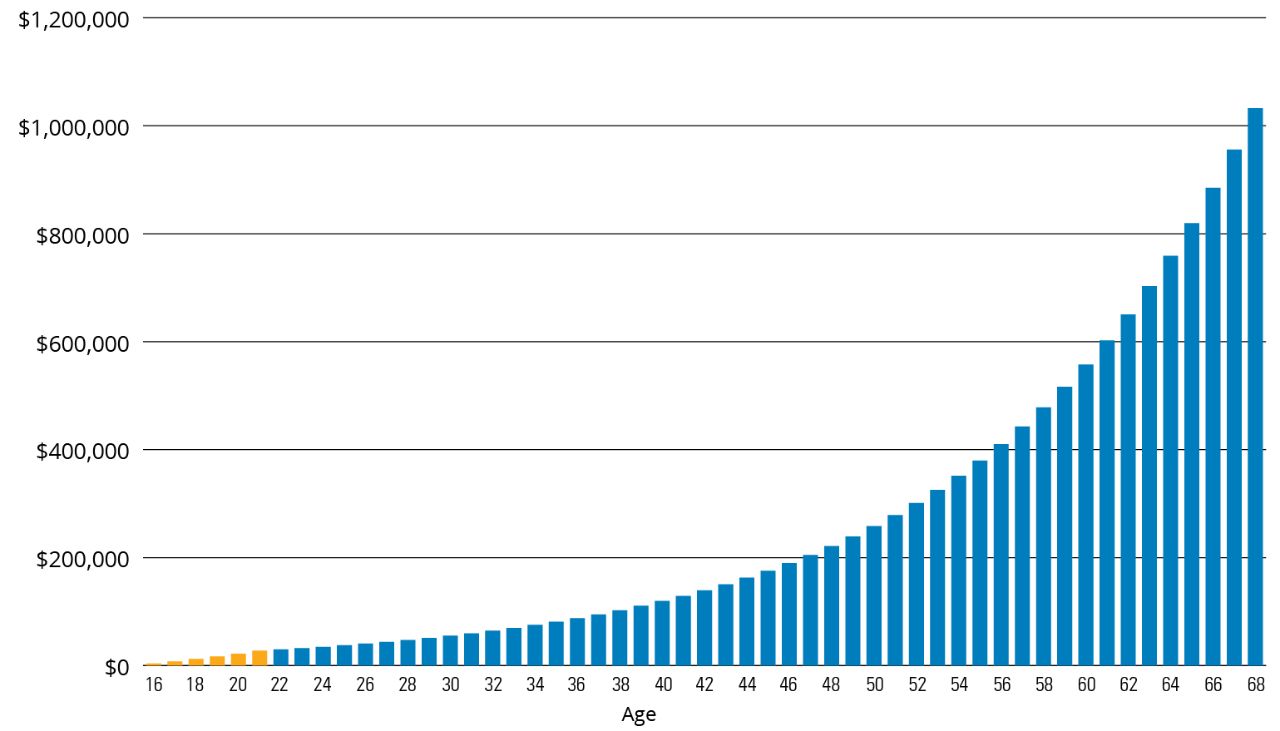

Just as importantly, investing early gives money more time to grow. Thanks to the power of compounding, even small contributions made in the teen years can potentially grow into a sizable nest egg over decades. This combination of habit-building and long-term financial growth makes early investing one of the most impactful steps a young person can take toward a secure future and a more comfortable retirement.