A growing number of families (59%) say they have a plan to pay for the full cost of college before a student enrolls, and 41% say they make the final decision about how to pay for college together.1 Has your family had this conversation?

Parents’ Role in Paying for College

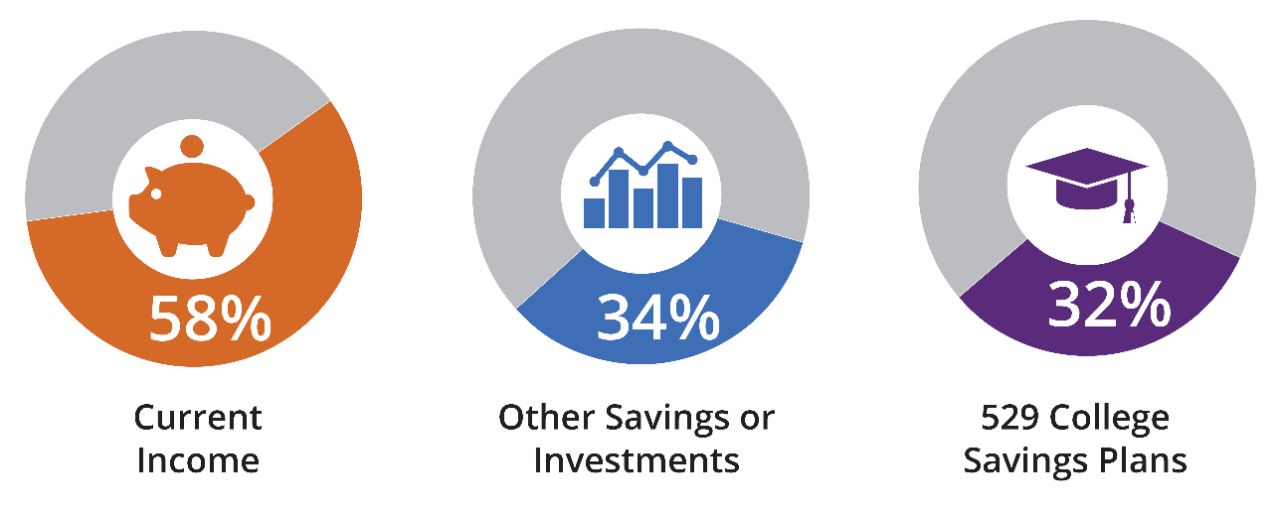

Most parents prioritize minimizing the cost of college for their child, and 74% help pay for their education.1 On average, parents aim to save $55,342 to help cover these costs.2 In addition to the average parental savings, most expect the cost of college to be a burden shared between parents and student.

On average, parents contributed roughly 38% of the total college education costs in the 2024-25 school year.1 The remainder is funded through a combination of student income, scholarships, grants, federal student aid, loans, and gifts from family. Even though many families are saving for college, 66% of families who borrow say that it was a key part of their college funding strategy.1

Setting Expectations With Your Future College Student

Paying for college works best when parents and children are on the same page. Creating a clear plan and being transparent about it can help make an overwhelming process feel more manageable—and allow you to work through decisions together.

An important first step, ideally starting in your child’s early school years and continuing through high school, is to consult with your financial professional. If you’re using a 529 plan, you’re already leveraging a tool designed to help families save more effectively than a traditional checking or savings account. A financial professional can also help you understand how to maximize the plan based on your family’s specific goals and circumstances.

The next step is to talk with your child about who will pay for tuition and fees before they begin the college application process. Do they understand what a 529 plan is? Will they apply for grants or scholarships? Have you discussed the potential cost benefits of public or in‑state schools or other ways to make college more affordable?

A 529 plan can provide a strong foundation for financing your child’s education, but it’s only part of the picture. Continue building on that foundation with open, honest conversations about goals, expectations, and affordability. And as plans take shape, check in with your financial professional to make sure your savings approach aligns with what your family hopes to achieve—and whether you’re on track to get there.