Newborns—the joys are limitless. Tiny fingers. Toothless smiles. The intoxicating new baby smell. But first-time and veteran parents alike know that limitless anxieties come along with having a new baby, too. One particular worry that looms large for today’s parents is the cost of college.

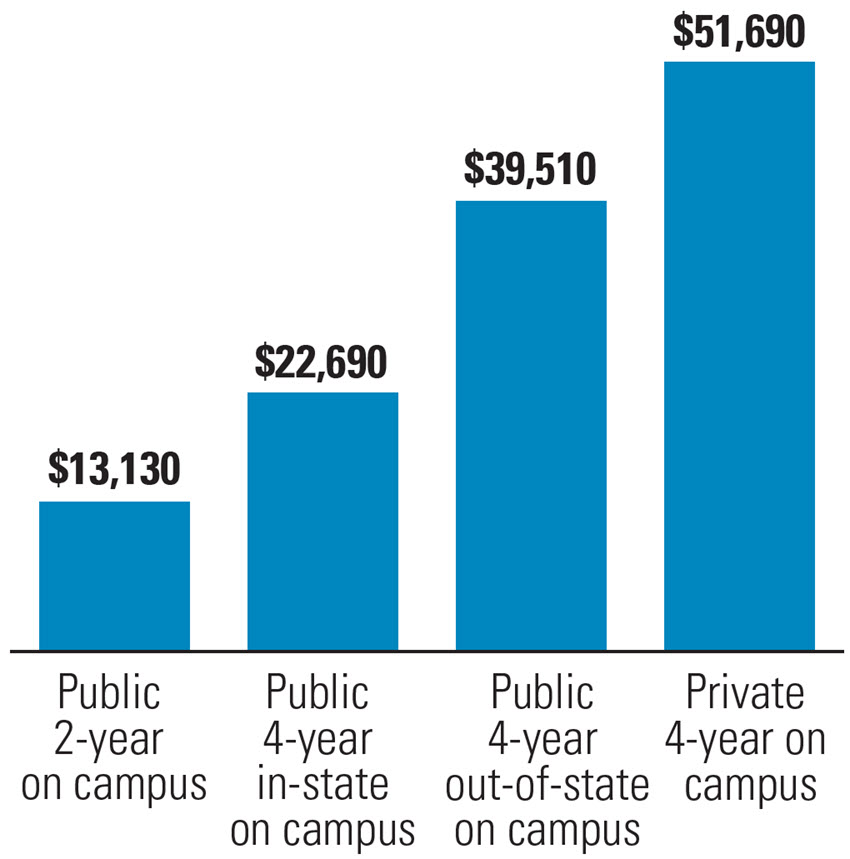

Tuition, room, and board today can cost anywhere from $23,000 to upwards of $52,000 at a four-year institution.1 Who knows what it will be

18 years from now? And with student debt in America totaling upwards of $1.75 trillion,2 how could new parents not be nervous?

The best way to save for your child’s college education? Start early.

Invest Early, Invest Often

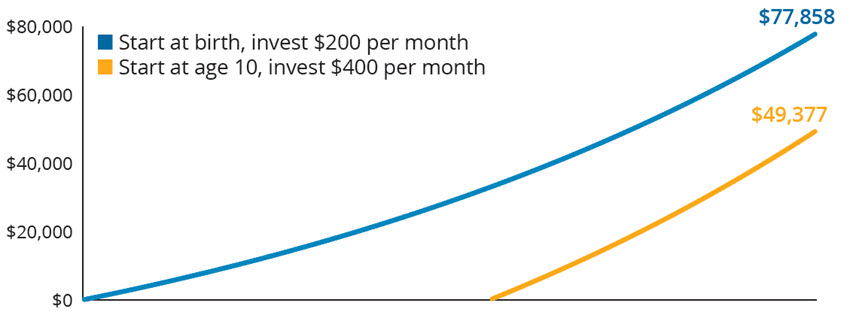

Parents of newborns and young children have one huge advantage when it comes to contributing to a 529 plan: time. This is the most valuable asset when it comes to long-term investments. By investing in your child’s education when they’re still young, you have a large window of opportunity to capitalize on potential compound interest. Even investing a modest sum may set your child up for success (after all, you have bibs and pacifiers and diapers—so many diapers!—to buy).

For example, if you invest $200 per month from the time your child is born until the day they turn 18, you will have accumulated nearly $78,000, assuming a 6% rate of return. Comparatively, if you begin investing $400 monthly beginning when your child is 10 years old, you will have amassed about $49,000 (also assuming a 6% rate of return). Investment returns are not guaranteed, and you could lose money by investing in a 529 Plan.